JHVEPhoto

Investing Thesis

Ever since I read Peter Lynch’s One Up on Wall Street, I have made it a habit to look at the writing on whatever packages I find lying around my house. This summer, in preparation for a minor surgery, I was scheduled to undergo, my surgeon’s assistant handed me a tiny bottle of acrid-smelling soap intended to disinfect the area upon which the doctor would operate. As I unwrinkled my nose following an ill-advised whiff, I rotated the bottle in my hand and saw that the soap had been produced by the McKesson Corporation (NYSE:MCK). Whether it was the heady olfactory effect wrought upon my staggering mind by the foul-smelling soap or simple curiosity, I decided to read up on the company and discovered a stock that could potentially fit nicely into my growing portfolio of dividend-paying equities.

It’s a Buffett Stock

One of the first things I found when seeking out information about McKesson was that Berkshire Hathaway (BRK.A, BRK.B) had initiated a position in the company by purchasing 2.92 million shares in the first quarter of the year. The Oracle of Omaha’s company added an additional 276 thousand shares in the second quarter, making McKesson one of Berkshire’s top 25 holdings.

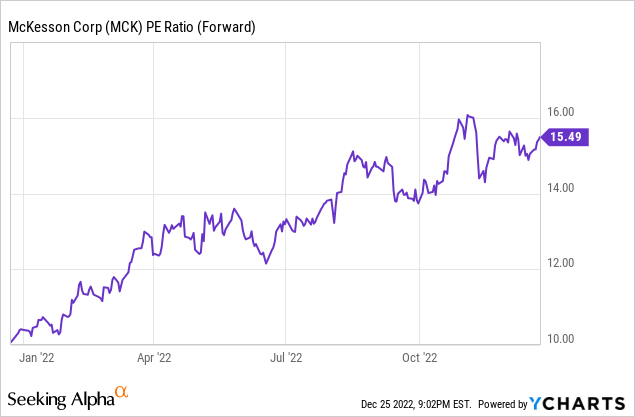

Given that Buffett has a well-earned reputation both for picking excellent companies trading below their intrinsic value and for favoring stocks that pay dividends, Berkshire’s newly-opened stake in McKesson struck me as a potentially positive sign. The first thing I looked at was MCK’s P/E ratio, which reveals a comparatively attractive valuation:

While Buffett appears to have swooped in when the company’s forward P/E was between 10 and 12, its present ratio of 15.49 is still quite a bit below the S and P 500’s 20 and suggests the company remains something of a bargain.

The Dividend

In July, McKesson raised its dividend by 15%. In the company’s press release announcing the hike, Brian Tyler, McKesson’s Chief Executive Officer declared that the “dividend increase demonstrates our continued commitment to returning capital to shareholders as part of our disciplined capital allocation framework” and “exemplifies the strength of our consistent cash flow generation and reflects our confidence in the long-term trajectory of the business.” In other words, McKesson is both committed to paying shareholders in the form of regular dividends and confident that it can continue doing so for the foreseeable future.

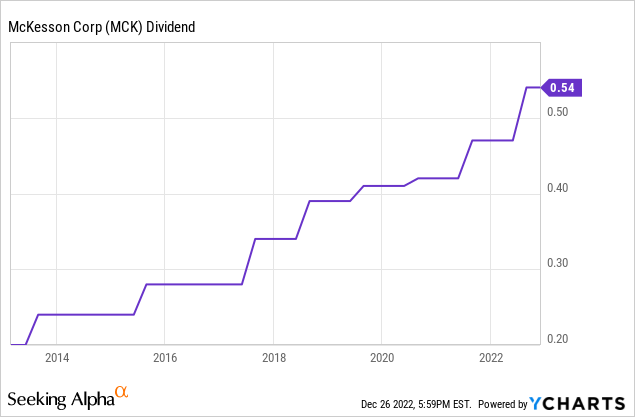

If you are looking for current income, however, McKesson is probably not the best company to buy. At the stock’s present price of $383.67, the $0.54 per share quarterly dividend amounts to a paltry 0.53% yield. For those of us willing to forgo a high current yield in an effort to produce a significant future income stream, on the other hand, McKesson offers some real potential.

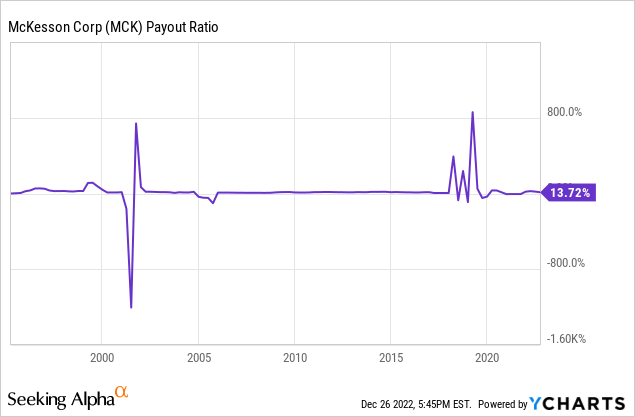

At the moment, McKesson’s payout ratio is just under 14%, which is right around the company’s historic level:

While maintaining its comparatively low payout ratio, McKesson has managed to raise its dividend for each of the past fifteen years. In the past decade alone, MCK’s quarterly dividend has climbed from $0.20 per share to $0.54:

During that ten-year span, McKesson has maintained a dividend growth rate of just under 10% annually, easily exceeding the rate of inflation during that time. Taken together, the low payout ratio, the company’s public commitment to returning capital to shareholders, and the pattern of regular dividend hikes suggest that McKesson is well-positioned to join the venerable ranks of Dividend Aristocrats in the next decade.

A Recession-Resistant Business

The anecdote with which I open this article highlights one of the most appealing aspects of McKesson’s business model: the company distributes pharmaceutical products to medical facilities. As many sage investors will tell you, buying companies tied to human needs during a recessionary environment is one of the more tried-and-true ways to stay invested during a bear market. After all, while people will likely cut back on luxuries and other non-essential expenses, we still need food, shelter, and medical care. Indeed, I had been cutting back on quite a few expenses at the time my surgery came up, but that was simply not something I could put off any longer.

Unlike some other companies in the health care sector, McKesson does not actually produce life-saving pharmaceuticals. Instead, the company focuses on distributing pharmaceuticals produced by other companies, providing health information technology, medical supplies, and care management tools to hospital networks both in the United States and, to a lesser extent, around the world. Importantly, McKesson delivers one third of all pharmaceuticals used in North America–and that market share provides the company with perhaps its greatest competitive advantage. One need look only as far as Operation Warp Speed’s decision to use McKesson as the distributor for Covid-19 vaccines in 2020 to see just how central the company is to meeting the nation’s medical needs.

Generating Profits Out of the Thinnest of Margins

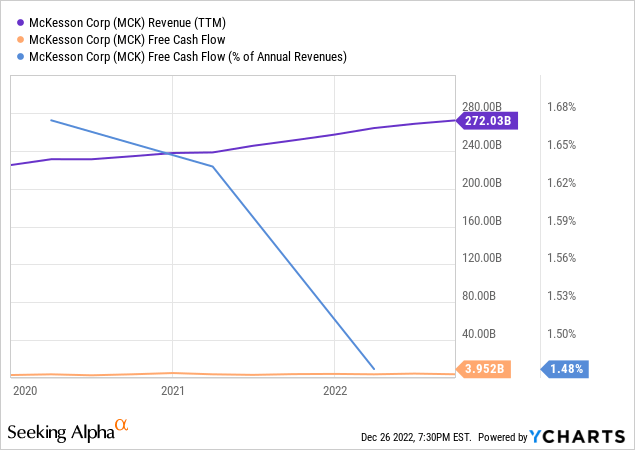

Given McKesson’s size, the company is able to operate in such a way as to undercut its competitors by generating significant profit out of the thinnest of profit margins. At present, McKesson reports just over $272 billion dollars in sales and just under four billion dollars in free cash flow, which is equal to 1.48%:

Not many companies can afford to take less than one and a half cents of profit for every dollar it makes in sales, but a large enough outfit can collect enough pennies to make it work. Ultimately, it is the company’s ability to operate at such a large scale that provides McKesson with its enviable ability to withstand competition.

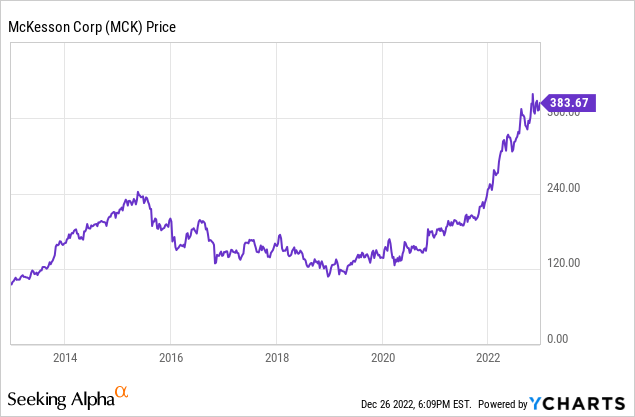

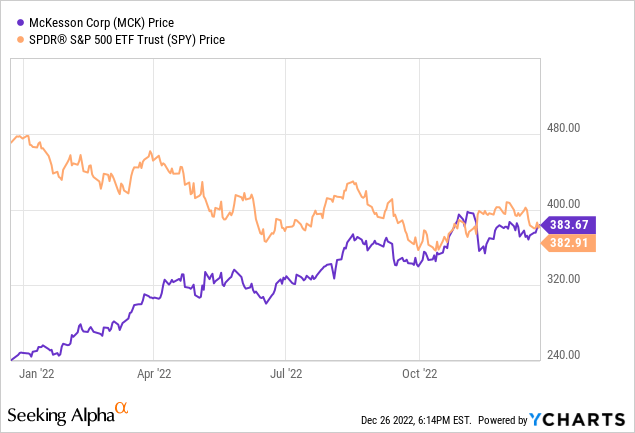

Share Price

As one might expect from a stock Warren Buffett favors, McKesson’s share price has performed quite well in the months since Berkshire Hathaway bought two tranches of MCK earlier this year:

In contrast with the SPDR S&P 500 (SPY), McKesson has enjoyed a steadily climbing share price all year:

While McKesson’s share price could certainly take a hit as we move forward into 2023, the fact that the company has steadily appreciated during the bear market of 2022 suggests that Wall Street takes a bullish stance on the company and may very well continue to do so.

Conclusion

As a major player on the distribution end of the health care industry in North America, McKesson Corporation is uniquely positioned to provide investors with both market-beating share price appreciation as well as a well-covered, steadily growing dividend. Between the company’s ability to generate meaningful profit out of the slimmest of profit margins, its central role in the distribution of life-saving pharmaceuticals, and its stated intent to return capital to shareholders, McKesson is a solid addition to dividend growth portfolio.

Be the first to comment