Khongtham/iStock via Getty Images

Investment Thesis

Dividend income stocks that come with a high Dividend Yield can enable you as an investor to gain an important amount of extra income, which can then be used to cover your monthly expenses.

Using an investment strategy with a focus on dividend income and dividend growth may help give you more control over your financials and to sleep better at night as it means that you don’t have to constantly look at your bank account to see if your stocks have gone up or down. Instead, you can look forward to regularly receiving additional income that can increase on an annual basis.

I consider it to be important to have a mix of companies that provide your portfolio with a high Dividend Yield and others that provide you with Dividend Growth. Building such a portfolio allows you to increase your additional income from year to year.

This article will focus on companies that can provide you with a relatively high Dividend Yield.

However, when seeking high yield dividend income stocks for your portfolio, you should be careful: a high Dividend Yield might be an indicator that the company’s dividend could be cut in the future, thus causing the stock price to decrease significantly. This could all result in your investment turning out not to be a good choice.

For this reason, I have selected 5 companies which I consider to be attractive, since they not only provide you with a relatively high Dividend Yield but they also have a relatively low Dividend Payout Ratio (which decreases the chances of a dividend cut) and have shown Dividend Growth over the past years (strengthening my belief that they should be able to raise their dividend in the upcoming years as well).

In addition to the characteristics mentioned above, these companies can also contribute to the diversification of your investment portfolio as each comes from a different industry.

The 5 companies I have selected for you are as follows:

JPMorgan

With Total Assets of $3,743.57B, JPMorgan is the largest bank in the U.S. and, at the same time, among the five largest banks in the world.

At the time of writing, JPMorgan pays its shareholders an attractive Dividend Yield [FWD] of 3.05%. When looking at the bank’s Dividend Growth Rate over the last 5 years, it becomes clear why I consider JPMorgan’s Dividend to be so attractive: the bank has shown an Average Dividend Growth Rate of 14.42% during this period of time. This attractive mix of dividend income with dividend growth makes JPMorgan such an appealing choice not only for dividend income, but also for dividend growth investors.

At this moment, JPMorgan has a P/E [FWD] Ratio of 11.36, which is 9.09% below its 5 Year Average P/E Ratio (12.50), indicating that the company is currently slightly undervalued.

JPMorgan shows a similar P/E [FWD] Ratio when compared to competitors such as Bank of America (NYSE:BAC) (P/E [FWD] Ratio of 10.23) and Wells Fargo (NYSE:WFC) (11.60). However, I believe that the largest bank in the U.S. deserves to be rated with a premium when compared to its opponents, particularly due to its diversification and strong brand value as well as the lower risk that comes attached to an investment in the company: JPMorgan’s 60M Beta of 1.13 indicates that the risk of investing in the bank is slightly lower than the risk of investing in competitors such as Bank of America (60M Beta of 1.39), Wells Fargo (1.16) or Citigroup (NYSE:C) (1.57).

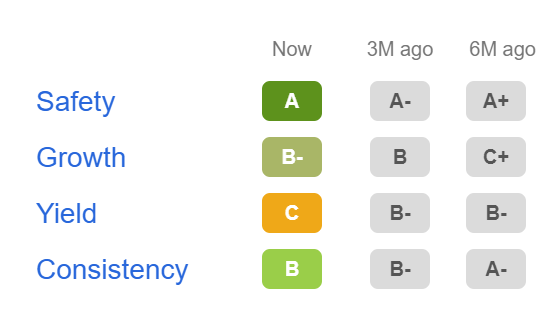

The Seeking Alpha Dividend Grades serve as an additional indicator to confirm that JPMorgan’s Dividend is appealing for dividend income and dividend growth investors: the company is rated with an A for Dividend Safety, a B for Dividend Consistency, a B- for Dividend Growth and a C for Dividend Yield.

Source: Seeking Alpha

Verizon

Verizon is among the largest companies within the Integrated Telecommunication Services Industry in terms of market capitalization ($161.31B) and revenue ($135.65B).

The company currently shows an attractive Dividend Yield [FWD] of 6.80%. This relatively high figure can be interpreted as being even more attractive when considering the company’s relatively low Dividend Payout Ratio of only 48.63%. This shows us that there is plenty of scope for future dividend enhancements and that the probability of a dividend cut is relatively low, at least with regard to the near future.

Even though I totally agree with those who claim that you cannot expect strong growth from the company in the upcoming years (it has shown an Average Revenue Growth Rate of 1.43% over the past 5 years); from my point of view, Verizon is an excellent choice to benefit from its dividend payments when holding the stock for a long period.

Due to the company’s high Dividend Yield [FWD] of 6.80%, selecting Verizon for your investment portfolio can also help you to raise the Average Dividend Yield of your portfolio. Its 60M Beta of 0.36 further indicates that you can reduce the volatility of your investment portfolio by investing in the company, helping to better prepare it for the next stock market crash.

Verizon has an EBIT Margin [TTM] of 19.73%, which is significantly higher than the Sector Median (9.25%), confirming the strong competitive position of the company within the Integrated Telecommunication Services Industry.

In addition to that, Verizon’s Return on Equity of 23.66% is significantly higher than its competitors such as AT&T (NYSE:T) (ROE of 11.92%) and T-Mobile (NASDAQ:TMUS) (2.22%), indicating that its management has a strong capacity for generating income from shareholder’s equity.

When it comes to Valuation, it can be highlighted that Verizon currently has a P/E [FWD] Ratio of 8.19, which is 52.22% below the Sector Median (17.15). At the same time, it is 28.02% below its Average P/E Ratio from over the last 5 years (11.38). Both statistics indicate that the company is currently undervalued.

Verizon’s Dividend Growth Rate [CAGR] over the past 10 years has been 2.47% and I expect this to continue in a similar manner during the years to come.

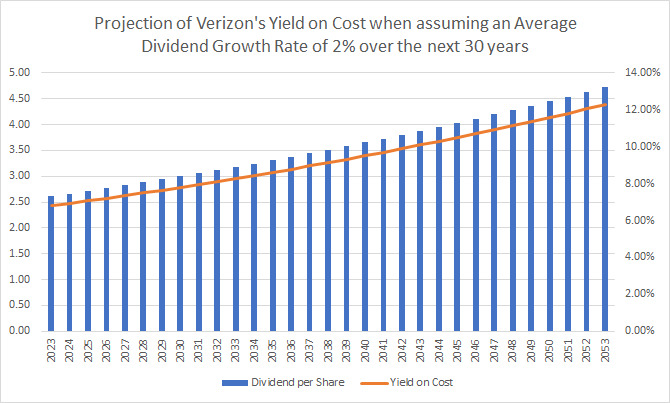

When assuming a Dividend Growth Rate of 2% for Verizon in the next 30 years, we would get the following results for the company’s Yield on Cost, which is shown in the graphic below, indicating again that it could be an excellent choice for your portfolio when investing with a long investment horizon and when planning to benefit from its slowly growing dividend payments.

Source: Seeking Alpha

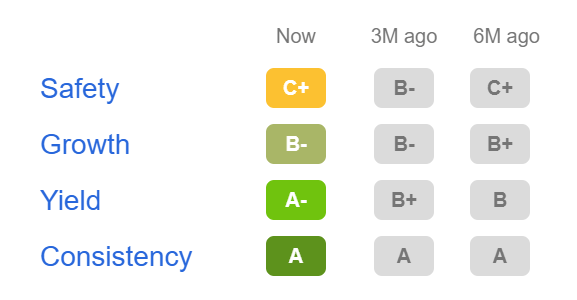

Verizon’s attractive dividend is underlined further by the results of the Seeking Alpha Dividend Grades. The company gets an A for Dividend Consistency and an A- for Dividend Yield. In terms of Dividend Growth, it receives a B- and for Dividend Safety, a C+.

Source: Seeking Alpha

Pfizer

I consider Pfizer to be a company that is attractive for both dividend income and dividend growth investors. My theory is based on several factors: Pfizer currently has a Dividend Yield [FWD] of 3.16% and, at the same time, has shown a 5 Year Average Dividend Growth Rate of 5.70%.

Furthermore, its Payout Ratio of 24.39% is low, indicating that the company should be able to continue to raise its Dividend to a significant amount in the coming years. In addition, Pfizer has shown 33 Consecutive Years of Dividend Payments and 12 Consecutive Years of Dividend Growth, thus reinforcing my belief that it should be able to continue doing so in the future.

Moreover, the company has a Free Cash Flow Yield [TTM] of 8.04%, which contributes to the fact that I consider it to be an excellent choice when it comes to risk and reward.

I also consider Pfizer to be an attractive pick for Valuation: the company currently has a P/E [FWD] Ratio of 9.10, which is 63.69% below the Sector Median, and at the same time this is 38.59% below its Average P/E Ratio from the past 5 years (14.82). These numbers strongly indicate that Pfizer is currently undervalued.

We can also see that its Valuation is significantly lower than its competitors such as Merck & Co., Inc. (NYSE:MRK) (P/E [FWD] Ratio of 19.19) or Novartis AG (NYSE:NVS) (20.67), reinforcing my theory that Pfizer is undervalued at this moment in time.

The company also shows attractive results when it comes to Growth: its Average EBIT Growth Rate [FWD] of 8.16% over the last 5 years as well as its Average EPS Diluted Growth Rate [FWD] of 10.15% over the same time period serve as indicators of this.

Pfizer’s high EBIT Margin [TTM] of 39.96% is a strong indicator of its competitive advantages and strong competitive position within the Pharmaceutical Industry.

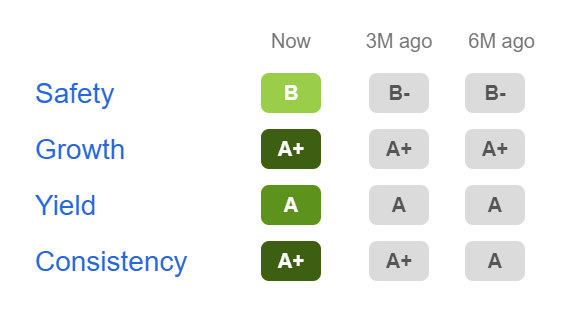

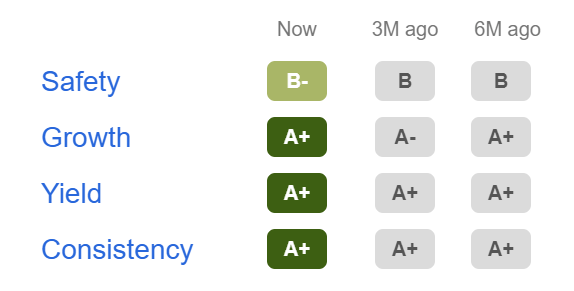

Below you can find the results of the Seeking Alpha Dividend Grades, which underline, once again, Pfizer’s very solid dividend: the company is rated with an A+ for Dividend Consistency and for Dividend Growth and with an A for Dividend Yield. For Dividend Safety, it receives a B rating.

Source: Seeking Alpha

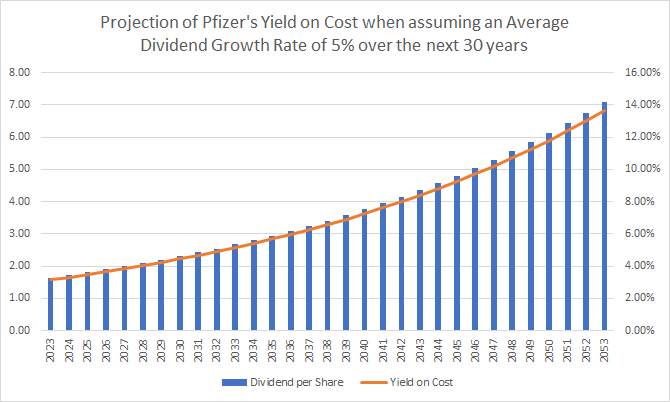

Below you can see the Yield on Cost for Pfizer when assuming an Average Dividend Growth Rate of 5% for the following 30 years: the graphic demonstrates that you could reach a Yield on Cost of 5.15% in 2033, 8.40% in 2043 and 13.68% in 2053. This strengthens my theory that Pfizer is an excellent pick for investors looking for dividend income and dividend growth at the same time.

Source: Seeking Alpha

Altria

Altria is part of this selection, because it currently provides shareholders with an attractive Dividend Yield [FWD] of 8.13%. Furthermore, Altria has been able to provide shareholders with 53 Consecutive Years of Dividend Growth, underlying that the company is a great choice for those who seek dividend income, but also dividend growth. Altria’s Dividend Growth Rate [CAGR] of 8.03% over the past 10 years serves as an additional indicator that the company is an excellent pick for dividend growth investors.

Altria’s P/E GAAP [FWD] Ratio of 14.72 shows us that the company is also attractive when it comes to Valuation: Altria’s P/E [FWD] Ratio is 27.88% below the Sector Median, at the time of writing. Altria’s current P/E [FWD] Ratio is also significantly lower than the one of Philip Morris (NYSE:PM), which shows a P/E [FWD] Ratio of 18.41, indicating once again that the company is currently undervalued.

When comparing Altria’s EBIT Margin [TTM] of 59.01% with the Sector Median (8.09%), it is confirmed that the company has an excellent competitive position within the Tobacco Industry: Altria’s EBIT Margin is 629.29% above the Sector Median.

Let’s take a look at the Seeking Alpha Dividend Grades in order to further evaluate the attractiveness of Altria’s Dividend: the company receives the highest possible rating of A+ for Dividend Growth, Dividend Yield and Dividend Consistency, once again underlining its rock solid dividend. For Dividend Safety, Altria receives a B- rating.

Source: Seeking Alpha

Exxon Mobil

Even though Exxon Mobil’s Dividend Yield is not as high as it has been in the past, which is mainly based on the fact that the company’s stock price has been up by 78% within the last 12 months period; I still consider it to be an attractive choice when investing with a long investment horizon and seeking companies that are able to provide you with constantly increasing dividend payments. Exxon Mobil’s current Dividend Yield [FWD] of 3.35% is 37.51% below its Average Dividend Yield [FWD] from the past 5 years (5.36%).

When it comes to Valuation, we can see that Exxon Mobil’s P/E [FWD] Ratio of 8.09 is in line with the P/E [FWD] Ratio of the Sector Median (8.22), providing us with evidence that the company is currently fairly valued. Furthermore, its P/E [FWD] Ratio is below the one of competitor Chevron (NYSE:CVX) (which currently has a P/E Ratio of 9.15). However, it is slightly higher than its European rival Shell (NYSE:SHEL) (which currently has a P/E [FWD] Ratio of just 6.04). This indicates that Shell could be the slightly better option if you are looking for an even more attractive company from the Integrated Oil and Gas Industry in terms of Valuation.

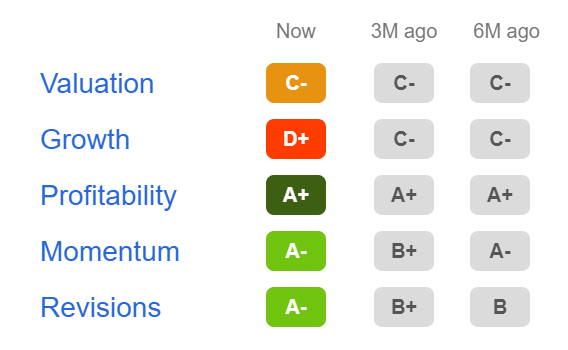

The Seeking Alpha Factor Grades provide us with further evidence that Exxon Mobil is currently still attractive despite its stock price having increased significantly over the past 12 months: the company receives an A+ in terms of Profitability and an A- for both Momentum and Revisions. For Valuation, it gets a C- and for Growth, a D+.

Source: Seeking Alpha

Conclusion

The companies, which I have discussed in this article, have a number of characteristics in common: they have a relatively high Dividend Yield, a relatively low Dividend Payout Ratio (which should provide each with the ability to further raise dividends in the upcoming years) and they have all shown significant Dividend Growth over the past years, thus increasing my confidence that they should continue to do so in the coming years.

In addition to that, they have significant competitive advantages over their competitors, strong financials and currently have an attractive Valuation.

Identifying these type of companies, which seem to be able to sustainably increase their dividends year after year, is important in order to keep increasing your additional income that you earn in the form of dividends.

Which are currently your favorite high yield dividend income stocks that, at the same time, provide the chance to significantly increase their dividend in the near future?

Be the first to comment