Panorama Images

Small-Cap Stocks vs. Large-Cap Stocks in 2023

Uncertainty in the markets, coupled with the Fed’s policy guidance, has prompted many investors to worry about growth prospects in 2023 and potential investment opportunities. Although retail sales fell 1.1%, and rents experienced a slight uptick of 0.8% month-over-month, the markets in the first 2-weeks of the year have reacted favorably, despite Fed officials emphasizing that rates will remain above 5%.

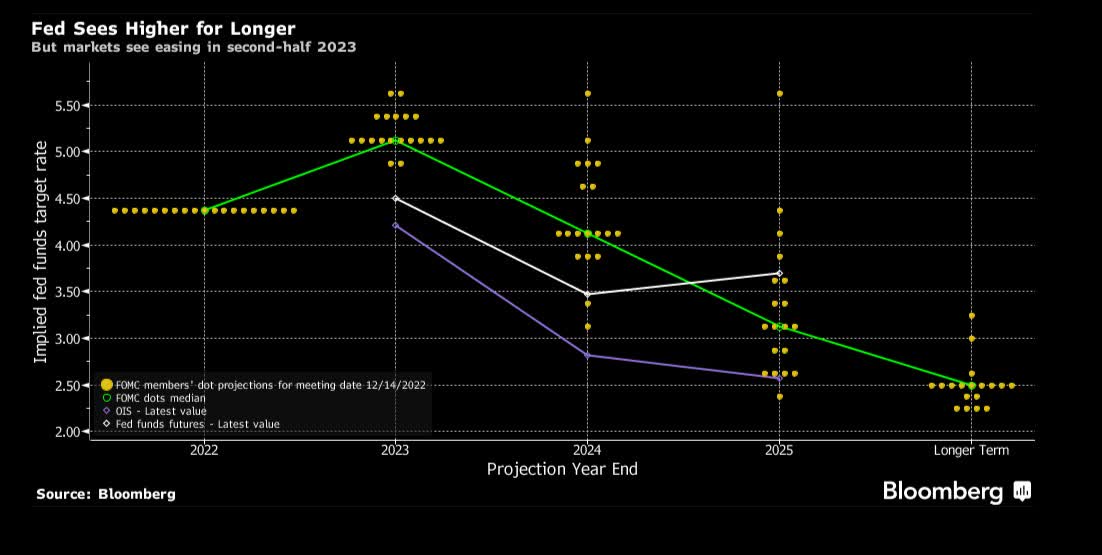

FED’s December 2022 Dot Plot

FED’s December 2022 Dot Plot (Bloomberg)

With small-cap stocks on the move, we’re focusing on getting in on the action by buying a few cheap stocks with small market caps. While stocks under $10 are typically small-cap, I’ve also included three stocks under $10 with large market caps. I’m neutral in terms of large- versus small-cap stocks, but if we see another leg down, small-cap stocks could sell off more than large-cap, presenting an opportunity to buy the dip. Longer term, if we see another reversal after the downturn or this current uptrend, we’re experiencing in 2023 holds, the expected return on the small-cap could expect to be better than the large-cap.

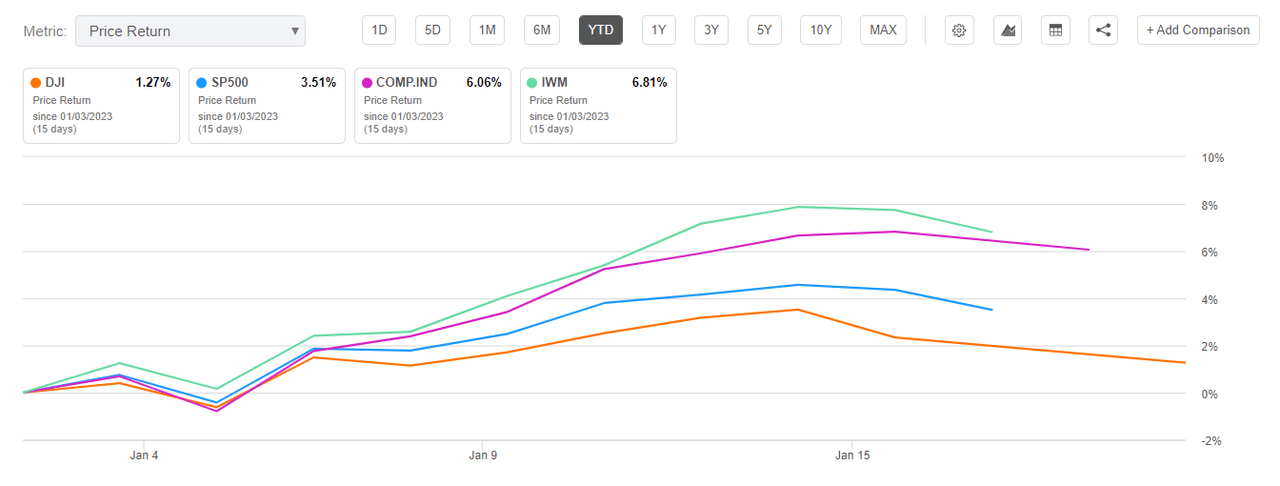

Small-Cap Stocks Outperform YTD to Kick-off 2023

Small-Cap Stocks Outperform YTD to Kick-off 2023 (SA Premium)

For over a decade, small-cap stocks have outperformed large-caps. To start the new year, iShares Russell 2000 ETF (IWM) is up 6.81%, outperforming the large-cap stocks YTD, as evidenced in the chart above, and small-caps are very attractive on a valuation basis. Typically smaller-sized companies with market capitalization between $300 million and $2B tend to be some of the more risky equity classes. In diversifying even further, my favorite picks for this article are all foreign stocks, quant-rated Strong Buys, and selected and sorted by market caps $1B or greater using a screen called Top Stocks Under $10. While I generally do not recommend stocks under $10, the key to smart investing is identifying stocks that possess strong fundamentals and, in this case, with low prices.

5 Cheap International Stocks Under $10 To Invest In

High inflation and negative macroeconomic factors make investing in the current environment difficult. Fluctuating currencies, high inflation, and interest rates pose challenges to many companies. Because small-cap companies tend not to be as profitable as larger ones, they typically go through high growth periods and possess higher leverage. In rising rate environments, this can pose problems to smaller companies with a lot of leverage, as they tend to sell off sharply when rising interest rates are threatened. Factor in fear of slowdown, recession, or contraction; small-cap stocks typically sell off more from a day-to-day trading perspective than large caps.

Because globalized economies are in a rut due to inflation, now may be a good time to seek out bargains, especially international stocks and/or emerging markets that have the potential to deliver upside over the long term. During periods of downturn, bargain hunting for attractive stocks along with collective financial traits like valuation, growth, EPS revisions, profitability, and momentum can pay off handsomely.

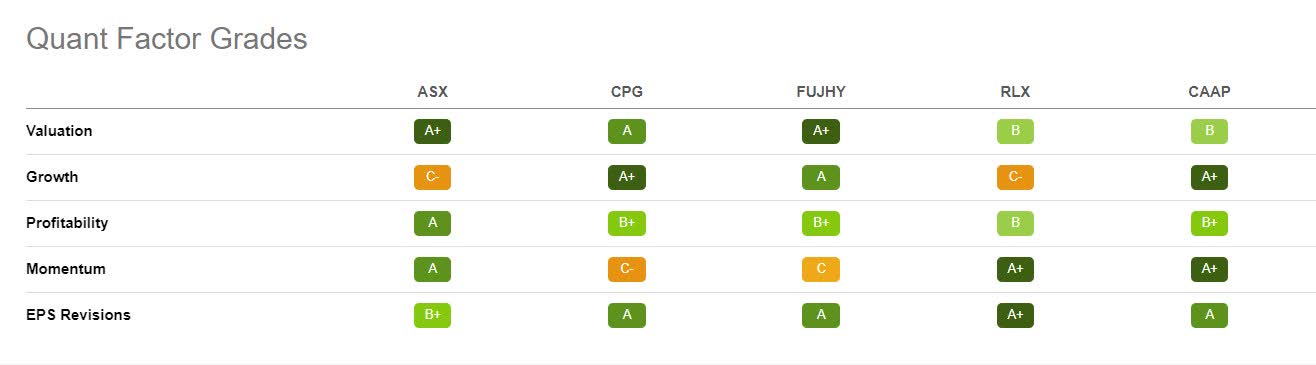

Each Stock Has Top Quant Grades On Fundamental Factors

Each Stock Has Top Quant Grades On Fundamental Factors (SA Premium)

Fidelity’s Asset Allocation Research Team forecasts that:

“International stocks will outperform US stocks over the next 20 years. Indeed, they expect even mature, developed markets such as Europe to outperform the US over that time. Those forecasts reflect the expectation that spending by consumers in EM countries will be a major source of economic growth and profits for companies over the next 20 years. EM stocks are estimated to be some of the best-performing stocks over that time partly because many EMs have relatively young and growing populations whose incomes will rise as their economies grow. India, for example, already boasts a greater number of households with disposable income of more than $10,000 than does Japan. The growth of these domestic consumer markets is a key reason why Fidelity’s Asset Allocation Research Team forecasts that EMs will grow to comprise about half of global gross domestic product in 20 years, compared with about 40% now and 25% 20 years ago.”

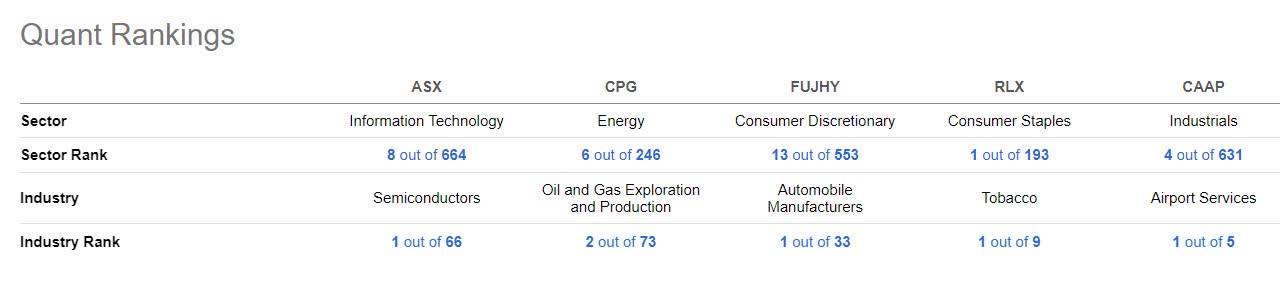

Each of Our Picks Quant Ranks At or Near #1 In Their Industry

Each of Our Picks Is At or Near #1 In Their Industry On A Quant Ranking (SA Premium)

With this in mind, along with our analysis showcasing the essential qualities found in my top 5 international stocks under $10, consider these strong buy stocks for a portfolio in 2023.

1. ASE Technology Holding Co., Ltd. (NYSE:ASX)

-

Market Capitalization: $14.26B

-

Quant Rating: Strong Buy

-

Price (as of 1/18/23): $7.11 per share

-

Quant Sector Ranking (as of 1/18/23): 8 out of 663

-

Quant Industry Ranking (as of 1/18/23): 1 out of 66

Connecting the digital generation, ASE Technology Holding Company offers advanced semiconductor packaging and testing, including 3D and flip chip ball grid array (BGA). With the advancements in 5G and smart digital applications, ASX offers electronic design and manufacturing services (EMS) and complex integration, including the development of engineering tests, wafer probing, modules, and materials, to name a few. Headquartered in Taiwan, ASX also has facilities globally and employs more than 95,000 worldwide. Given the popularity of semiconductors and strong demand, it makes sense that ASX has managed to grow despite market volatility. Trading at an extreme discount with bullish momentum, ASX is a tech stock primed for a portfolio.

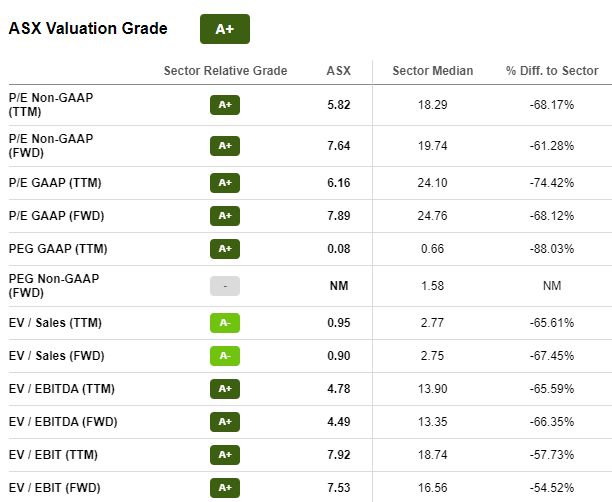

ASE Technology Stock Valuation & Momentum

Trading under $10/share, ASX is strongly bullish, with investors actively purchasing shares to drive the price higher, with many analysts calling the stock overbought. Although the stock is -7.54% over the last year, it beat the sector and S&P 500, and the stock is on an uptrend, starting the new year +13% YTD. ASE Technology’s forward P/E ratio is 7.89x compared to the sector median of 24.76x, nearly 70% below the sector median; the trailing PEG ratio is strong at 0.08x, an -88% difference to the sector.

ASX Valuation (SA Premium)

Despite geopolitical concerns and an environment riddled with supply chain constraints, ASX produced solid earnings, maintained free cash flow, and increased its dividend. With bullish momentum, the stock’s six-month price-performance is up 1,390%. As we await the official Q4 2022 Earnings figures being released at month-end, preliminary December net revenue is down approximately 19.2% Y/Y. However, FY revenues are up 10.7%. Although there are supply shortage constraints and risks that have affected the industry as a whole, there are many pros to consider if adding ASX to a portfolio that can serve as tailwinds to help its growth and profitability.

ASX Growth & Profitability

Despite the global recession risk in 2023, the bulls and my quant ratings indicate ASX is a strong buy, and improving supply chains can serve as tailwinds. Despite currency fluctuations and higher costs amid an unfavorable macro environment, ASX was able to offset the impacts given its local currency depreciation and passing higher costs off onto consumers. Last year was rough on many stocks, especially tech, and ASX bottomed in early July, trading at $4.45 but has managed to recover, trading near its 52-week high of $7.82.

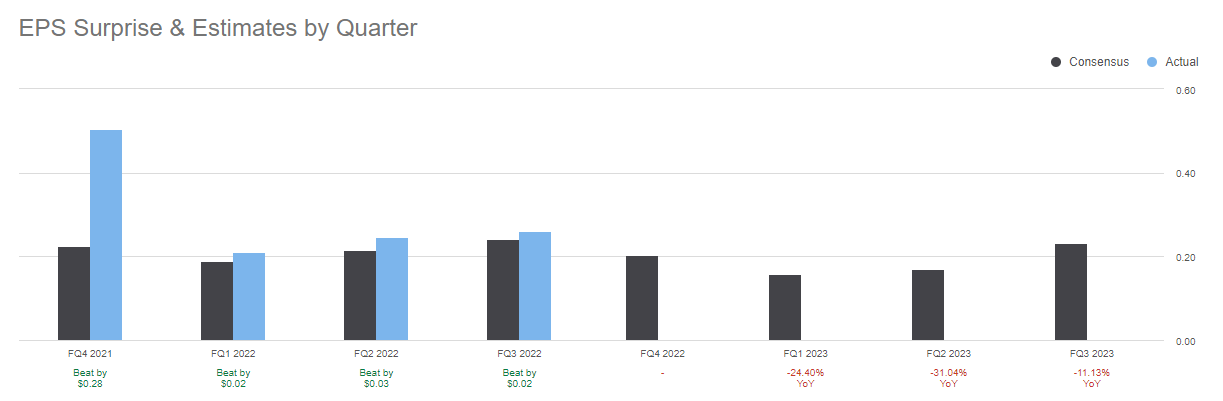

ASE Technology EPS

ASX Stock EPS (SA Premium)

Although we are awaiting Q4 earnings that may not be as solid as its most recent consecutive top- and bottom-line earnings beats, ASE Technology showcases continued strength and momentum and record ATM business revenues for Q3.

Third quarter EPS of $0.26 beat by $0.02, and revenue of $5.88B beat by $290.30M (8.5% Y/Y). Despite the slowing business environment, ASX’s overall profitability increased, and it managed to deliver record revenue and operating profits for both ATM and EMS business units. Offering an ‘A’ Profitability grade, a solid balance sheet, and nearly $3B in cash from operations, ASX is prepared for a potential slowdown or “normalized pricing environment” for 2023. When asked about next year and the company’s inventory controls and pricing, ASE Technology’s CFO, Joseph Tung, states:

“It’s going to be a normalized pricing environment. And there will be price hikes throughout the year. Our position does give us better pricing capability when we start the negotiation process, and we believe that we will have the capability to come up with a suitable pricing strategy that works for both ourselves and our customers. We do believe, and we remain very confident, that the margin that we’re going to have will move up from previously between cycles, 20% to 25%, now to mid-20 % to 30%. So we remain confident that we will have a structural margin improvement.”

With expected growth and better profit margins, ASX offers strong fundamentals in a popular industry used for everyday products worldwide, substantiating its Strong Buy rating.

2. Crescent Point Energy Corp. (NYSE:CPG)

-

Market Capitalization: $4.02B

-

Quant Rating: Strong Buy

-

Price (as of 1/18/23): $7.21 per share

-

Quant Sector Ranking (as of 1/18/23): 6 out of 246

-

Quant Industry Ranking (as of 1/18/23): 2 out of 73

Crescent Point Energy Corp. has been one of my top energy stocks since early 2022, offering tremendous metrics, upside in the sector, growth, and cash flow. A Canadian-based crude oil and natural gas company in western Canada, CPG, is drilling home the results. Offering high-return resources and generating significant excess cash flow is estimated to reach $1.25B in 2023 at $80 WTI based on annual production of 138,000 to 142,000 boe/d. CPG’s third-quarter success led to a special dividend of CAD 0.035 (USD .026) per share in addition to its regular CAD 0.08 dividend, and Crescent Point raised its full-year CAPEX outlook.

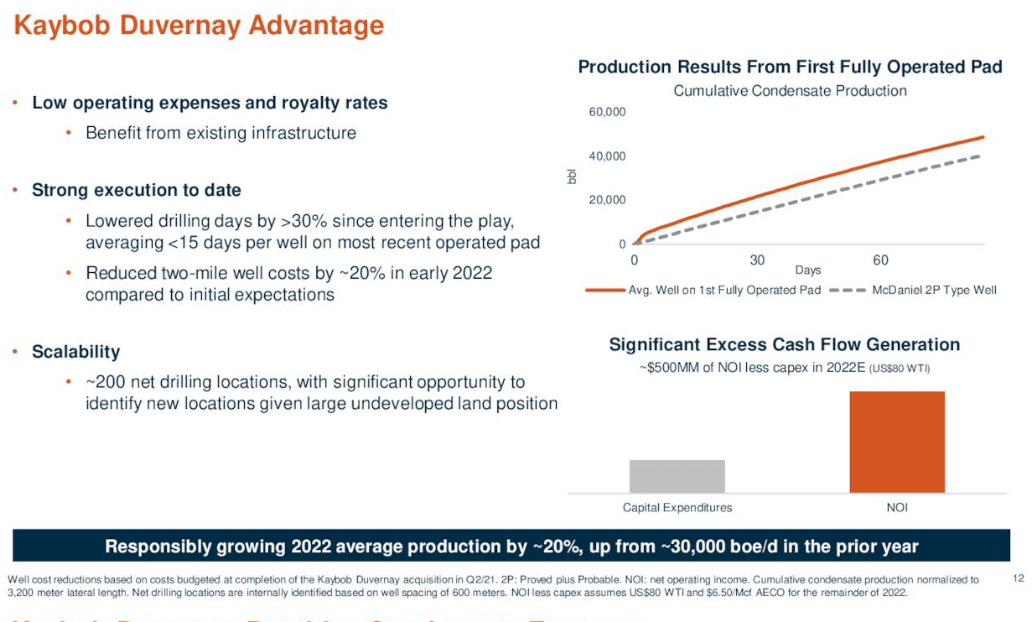

CPG’s acquisition of Shell Canada Energy’s Kaybob Duvernay assets has offered significant excess cash flow and opportunity for growth, profitability, and dividend yields.

Kaybob Duvernay Production Details (CPG Investor Presentation)

The initial acquisition was so successful that CPG recently announced an additional 130 Kaybob net locations. The addition will increase its base dividend by 25%, returning significant capital to shareholders, including 50% discretionary excess cash flow.

“We continue to generate strong full cycle returns from our Kaybob Duvernay assets, which are top quartile within our overall portfolio. Through this acquisition, we are increasing our drilling inventory in the play to over 20 years based on current production. In addition, our land position will increase to approximately 400,000 net acres. We are also adding base production with an estimated net present value of approximately $200 million at current strip commodity prices. The acquisition includes an attractive ESG profile consistent with our existing Kaybob Duvernay assets, including low emissions intensity and minimal asset retirement obligations,” said Craig Bryksa, President and CEO of Crescent Point.

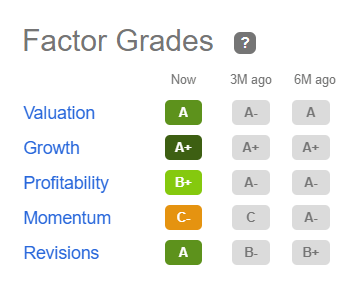

I chose this stock because it has strong factor grades, which rate investment characteristics on a sector-relative basis. In addition to strong growth and profitability grades, CPG is undervalued, highlighted in its valuation framework. With an ‘A’ valuation grade, CPG is trading more than 70% below its sector, with a forward P/E ratio of 2.49x and a strong forward EV/EBITDA. Below, the Growth and Revisions Grades indicate that CPG has excellent potential and is fundamentally sound compared to the sector. With A+ Growth and A+ Earnings Revision, CPG is one of the fast-growing companies in its sector.

CPG Factor Grades

CPG Stock Factor Grades (SA Premium)

Not only have there been five upward analyst revisions over the last 90 days and zero downward, as energy prices remain elevated and CPG maintains $1.52B cash on the sidelines. Consider riding the momentum of this stock considered strongly bullish, as investors actively buy shares, resulting in analysts calling the stock overbought.

3. Subaru Corporation (OTCPK:FUJHY)

-

Market Capitalization: $11.92B

-

Quant Rating: Strong Buy

-

Price (as of 1/18/23): $7.94 per share

-

Quant Sector Ranking (as of 1/18/23): 13 out of 553

-

Quant Industry Ranking (as of 1/18/23): 1 out of 33

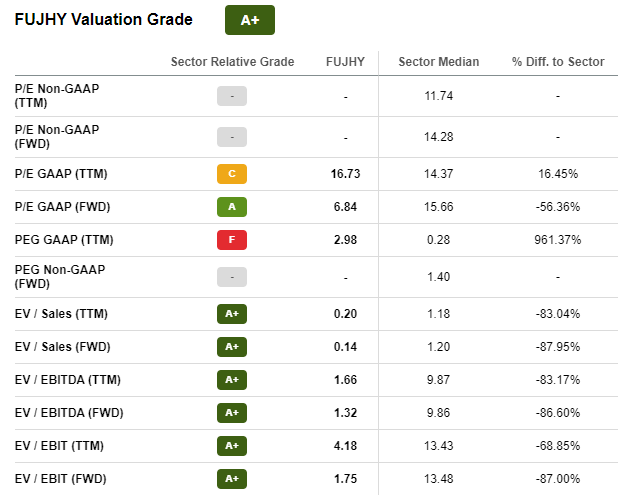

The automobile industry has been on quite the rollercoaster ride since the pandemic. Rallying to highs on the heels of demand that manufacturers could not keep up with, followed by lows amid semiconductor shortages, lockdowns, and macroeconomic factors that have still not fully worked themselves out. But Subaru Corporation has remained resilient. Despite falling 15% over the last year, the stock remains quant-rated a strong buy. Subaru trades at a significant discount, showcasing an A+ overall valuation grade. Forward P/E ratio is 6.84x, a more than 56% discount to the sector, forward EV/Sales and EV/EBIT with more than 87% discounts to its sector peers, and bullish momentum.

FUJHY Valuation Grade (SA Premium)

Offering strong financials that include a net cash position 50% over the market cap (as of November 4, 2022), production and profit increases are anticipated to continue into the new year. The Japanese brand, known for quality and reliability, is anticipated by analysts to have strong revenue growth for 2023 and 2024 and projected revenue for FY23 of 38% and 10% for FY2024.

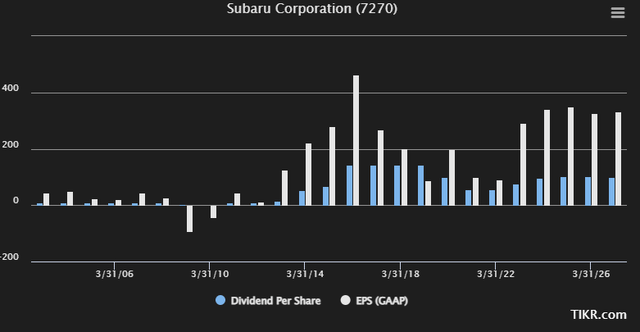

Consolidated revenue for Q2 FY23 increased 30.5% Y/Y, with profits increasing nearly 51% Y/Y. And as global economies anticipate slowing, which can lead to decreases in sales and consumer discretionary spending, Subaru has displayed signs that they are at risk of cutting their dividend. A few words on their volatile dividend history. Seeking Alpha likes to alert investors when a company’s dividend is at risk of performing badly by displaying a warning banner.

Subaru has traditionally offered an inconsistent semi-annual dividend, so if you’re looking for a company explicitly offering a regular dividend payment, consider our Top Rated Quant Dividend Stocks. Notwithstanding, as Wolf Report writes,

“The company’s shareholder dividend has been an interesting story to follow – and it’s one that’s likely to improve for the next few years if you’re to believe the analysts forecasting the business. As you can see, recent results for the company have been positive – and 2022 will be a down year, but 2023 forecasts are significantly better. Other analysts’ forecasts and the company’s quarterlies have been in line with these expectations.”

Subaru EPS/Dividends (TIKR.com)

Despite ongoing supply chain challenges, Subaru has shown continued strength. It is guided by and capitalizes on making positive impacts in the world and markets to its community commitment, which in turn aids in its vehicle sales that experienced an +11% jump in December, building the case for a strong buy company for 2023.

4. RLX Technology Inc. (RLX)

-

Market Capitalization: $4.04B

-

Quant Rating: Strong Buy

-

Price (as of 1/18/23): $2.59 per share

-

Quant Sector Ranking (as of 1/18/23): 1 out of 193

-

Quant Industry Ranking (as of 1/18/23): 1 out of 9

RLX Technology Inc., together with its subsidiaries, is a Chinese e-vapor product company that researches, develops, and sells tobacco products. Whether there’s a recession or no recession, a slowdown is anticipated for 2023, and people use tobacco products in good and bad times. Offering strong fundamentals and a $2.2B cash hoard, RLX is a strong buy consideration for portfolios undervalued at a mere $2.59 per share.

RLX Valuation & Momentum

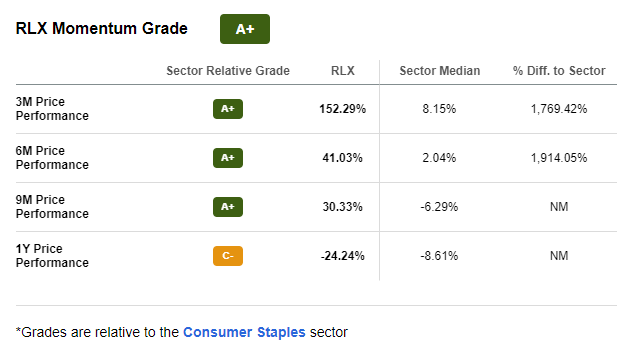

With a forward P/E ratio of 16.67x versus 20.93x and trailing PEG of 0.15x compared to the sector median of 0.65x, RLX trades at a discount and offers bullish momentum. Although the stock’s one-year price performance is -30%, it is on an uptrend, with a six-month price performance of +35%. The momentum grade below shows that RLX outperforms its sector median peers quarterly.

RLX Momentum Grade (SA Premium)

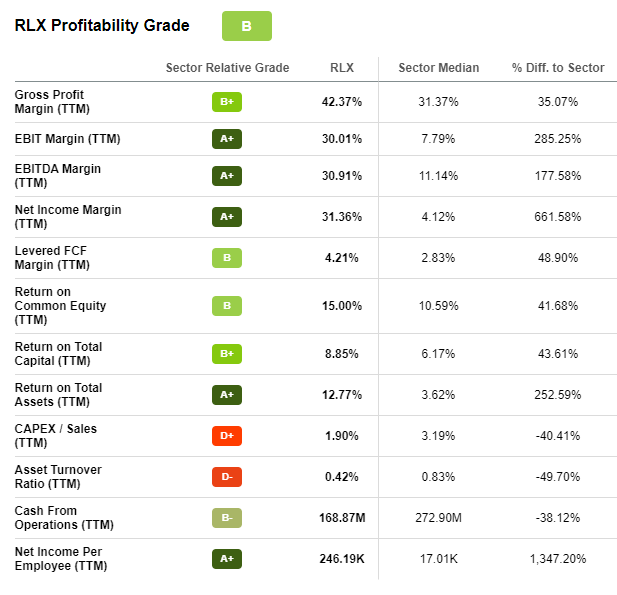

Although vaping comes with health risks, from an investment stance, there are also legal aspects, warning labels, flavor banning, and overall regulation and taxation, to be considered when investing in e-cigarette companies. It has expanded its product portfolio and geographies to alleviate some of the c consumption tax that will affect RLX. RLX has also improved operational efficiency and standards by discontinuing older products to meet regulations. Overall strategic changes have resulted in a 30.9% quarter-over-quarter decrease in non-GAAP operating expenses and Q3 net revenues of RMB 1.0B (USD ~$150M).

RLX Stock Profitability (SA Premium)

Strong growth and profitability grades delivered Q3 gross margins of 50% compared to the same period last year of 39.1%. As RLX Chief Financial Officer Chao Lu states:

“We remain confident that our business’s resilience and operational excellence will empower us to navigate the challenges as we explore new opportunities for growth and development. Meanwhile, we believe all industry participants across the value chain will work jointly to overcome this challenging time and adapt to the paradigm of the new era.”

With China’s smoking rate above 25% and smokers persisting globally, RLX is a unique consumer staple with strong overall metrics, along with my final pick from Luxembourg, Corporación América Airports S.A.

5. Corporación América Airports S.A. (CAAP)

-

Market Capitalization: $1.59B

-

Quant Rating: Strong Buy

-

Price (as of 1/18/23): $9.88 per share

-

Quant Sector Ranking (as of 1/18/23): 4 out of 631

-

Quant Industry Ranking (as of 1/18/23): 1 out of 5

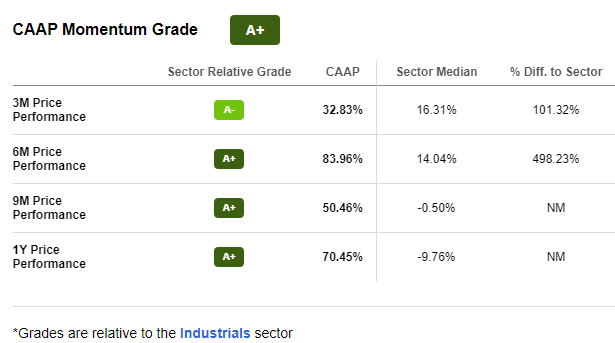

Headquartered in Luxembourg and operating 53 airports in six countries across Latin America and Europe, Corporación América Airports S.A. is a leading private airport operator through its subsidiaries. Despite the bouts of negativity surrounding airlines and the industry since the pandemic, CAAP is on a bullish trend, with a 200-day moving average that is upward-sloping. Not only is the stock’s bullish momentum causing investors to purchase shares actively, but CAAP’s passenger traffic is also at 87.4% of pre-pandemic levels, which included a 34.5% Y/Y increase in November.

CAAP Stock Momentum Grade (SA Premium)

CAAP is trading near its 52-week high of $10 but comes at a discount with a forward P/E ratio of 12.51x, a -35.02% difference to the sector. Although CAAP’s forward Price/Sales is a modest 1.13x compared to 1.32x, based on current revenues, CAAP is showcasing the ability for tremendous upside. As Marketplace author Ian Bezek writes:

“CAAP is going to produce more than $1.5 billion of revenues in 2023 against a market cap of $1.4 billion. Over the longer term, airports tend to earn at least 50% EBITDA margins and can get close to 70% with capable management and favorable concession agreements. Airports are natural monopolies and have consistently grown at several times global GDP…CAAP stock is still profoundly mispriced at $9. Admittedly $9 is a slightly less egregious valuation than $6 last quarter or $2/share back in 2020. But this is still a global airport empire selling at far below any reasonable calculation of its fair value today, to say nothing of where it will be as its growth projects and acquisitions bear fruit.”

CAAP Stock Growth & Profitability

CAAP posted record levels of robust top-and-bottom-line results for Q3 2022. In addition to a 78.6% Y/Y increase in passenger traffic that reached 18.7M, CAAP’s consolidated revenues of $395.5M was a whopping 111.6% Y/Y increase. Adjusted EBITDA of $131M was driven by success across business units and geographies. As post-pandemic recovery continues, CAAP staff anticipates increases in passenger traffic across all airports. They will focus on adding more routes for value creation and seeking greater investment opportunities. Where the stock is +72% over the last year, it continues upward, +13% YTD. With excellent factor grades and an industry primed for recovery, Corporación América Airports may be flying high in 2023, along with our previous four picks.

Consider 5 Cheap Stocks Under $10

Like U.S. stocks, international companies have been affected by high inflation, rising interest rates, geopolitical concerns, and slowing economic growth. In addition to the war in Ukraine, further challenges include potential increasing headwinds from China, lower-than-expected profits from companies around the globe, supply chain issues, volatile energy prices, and central bank tightening. Because these issues are well known, many of the factors may be discounted in the small-cap segment, and this may lead to bargains in the new year.

In my opinion, undervalued small-cap stocks with strong growth potential can offer upside in the new year. And although some small caps have fewer profits on the books compared to large caps, those with strong investment fundamentals and solid balance sheets, as showcased by our Quant System, can offer the risk-reward needed for portfolios. NWG, CPG, FUJHY, RLX, and CAAP are five unique companies that may help to diversify your portfolio into the new year. If international stocks do not fit your risk tolerance, you can choose from many more Top Stocks Under $10.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment