Lari Bat/iStock via Getty Images

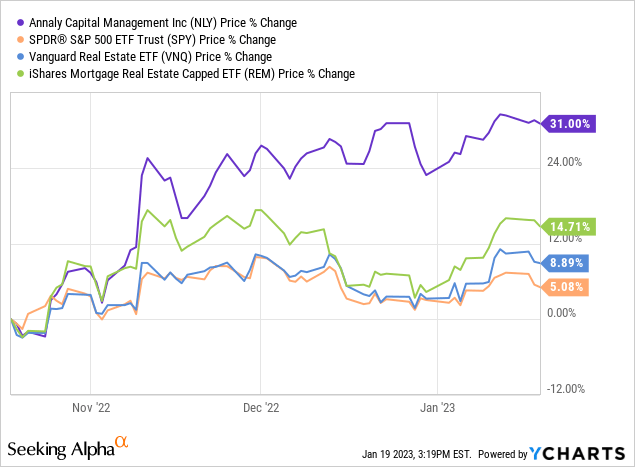

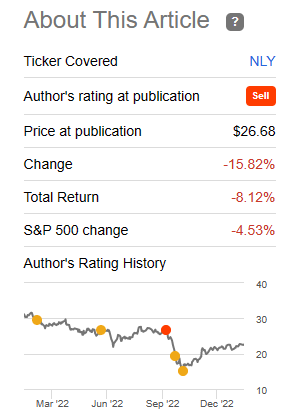

Annaly Capital Management Inc. (NYSE:NLY) has had quite the run in the last three months. The 31% price gain has put the broader market tracking SPDR S&P ETF (SPY) and the Vanguard Real Estate ETF (VNQ) to shame. It has even done far better than its brethren in the iShares Mortgage Real Estate Capped ETF (REM).

That rebound was almost enough to wipe out all the unhappy memories of 2022. Almost, but not quite. We tell you three reasons why you should look beyond this rebound and consider exiting the shares while the going is good.

The Company Is Expensive

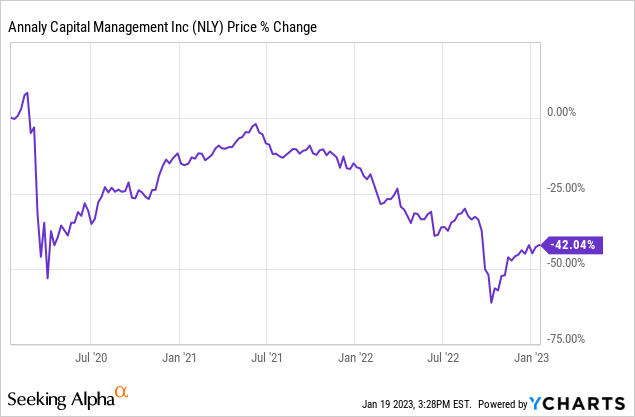

Investors tend to be price sensitive. That price memory is what creates “support” and “resistance” on technical analysis. That price memory also tells people that NLY is “cheap” today. After all the stock is down 42% over the last three years and still very much in the bottom end of its range.

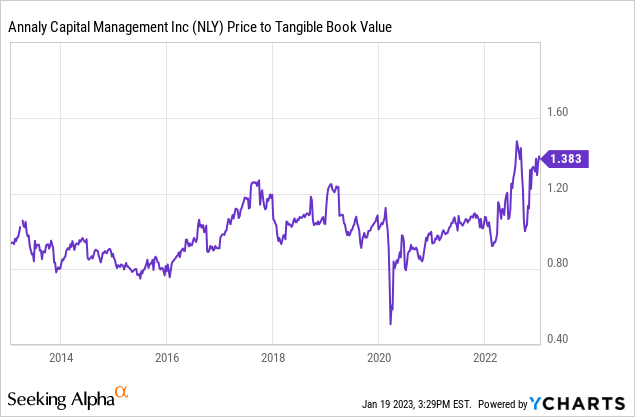

But that has nothing to do with cheap. Mortgage REITs like most financial stocks, should be evaluated in relation to tangible book value. Based on that metric NLY is trading rather expensive relative to its history.

One point to note here is that the chart is based off the Q3-2022 numbers. The current market rebound and improvement in the mortgage-treasury spreads does bode well for tangible book value. But even adjusted for that, we think NLY is at least at a 10% premium today. In the climate we are in, with risk-free rates approaching 5%, a good discount to book value is warranted for NLY. Ideally investors should look to buy this at under 15% discount to tangible book value.

Curve Inversion Will Compress Earnings In Back Half Of 2023

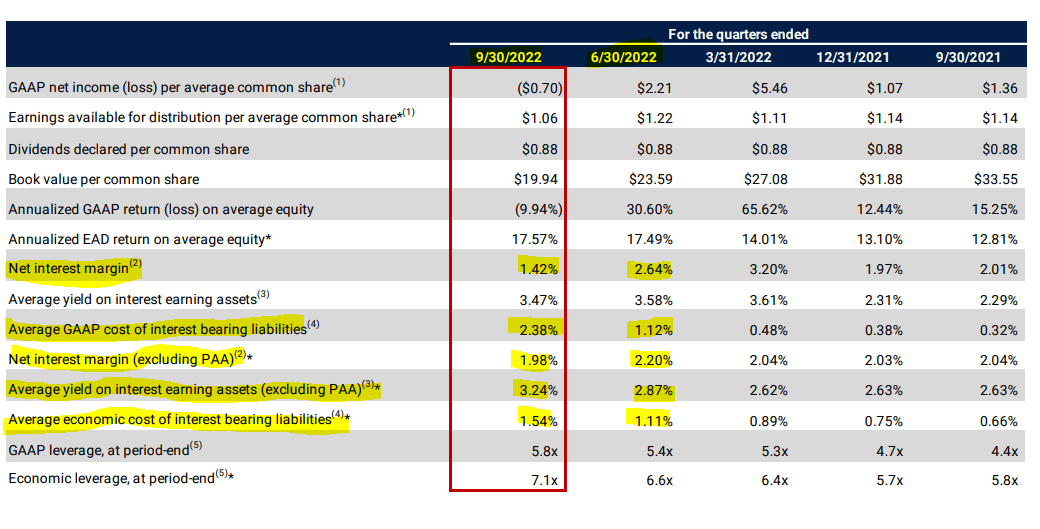

While the focus has been on the extraordinarily high spreads new mortgage backed securities offer vs 30-year treasuries, that won’t be the driver for cash flow. The real driver will be the existing mortgage backed securities held on NLY’s balance sheet versus the short term interest rates. We saw this in Q3-2022, where all measures of interest expense went up and all measures of net interest income fell.

NLY Q3-2022 Presentation

Thanks to the hedges on NLY’s books we did not see the full impact of those earlier rate hikes. 2023 will be vastly different. NLY will also have extremely low prepayments with which to reinvest in higher yielding mortgage backed securities. Navigating this will be complex and as we shall see in point three, NLY has not done that very well even when things have been favorable.

Mortgage REITs Are Poor Allocators Of Capital

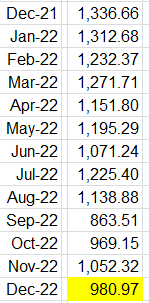

While the above statement applies at every single moment, it takes on more significance when there is financial turmoil. Mortgage REITs in general and NLY in particular create higher risks when things go south. For Mortgage REITs, we can use the data from NAREIT. You can download the file and verify this for yourself. Below are the total return index value. This includes those huge distributions everyone loves so much. As you can see the total return index ended December 2022 at 980.97.

NAREIT

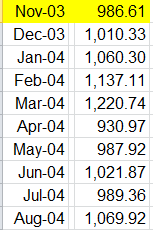

What might impress the reader is the fact that the mortgage REIT index first hit this level in (you better be sitting for this), November 2003.

NAREIT

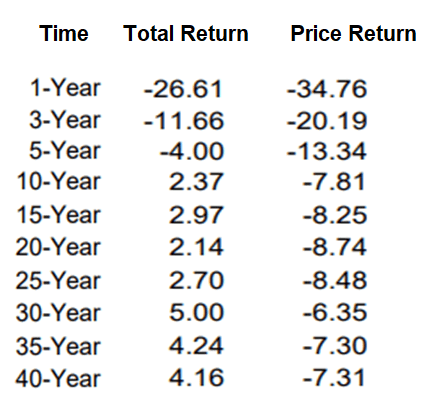

If the total return remains unchanged until November, we will have 20 years of literally zero returns. Actual 20-year returns are currently a bit better and total 2% a year. Here is the performance for the sector for the past 40 years.

NAREIT

Price returns are a total horror show. Total returns save the day but if over 25 years the return is 2.7%, one really has to wonder what is going on in the sector. We will add here that those returns are likely ahead of actual returns achievable as they don’t have fees. iShares Mortgage Real Estate Capped ETF (REM) has a 0.48% annual fee which would reduce your returns quite substantially. There are also taxes on distributions which can be quite substantial. Remember that you are paying taxes on the entire 10-15% yield, even though your total return may be 2%. Finally a lot of mortgage REITs get thrown out of the index. This is what the best mortgage REITs have delivered.

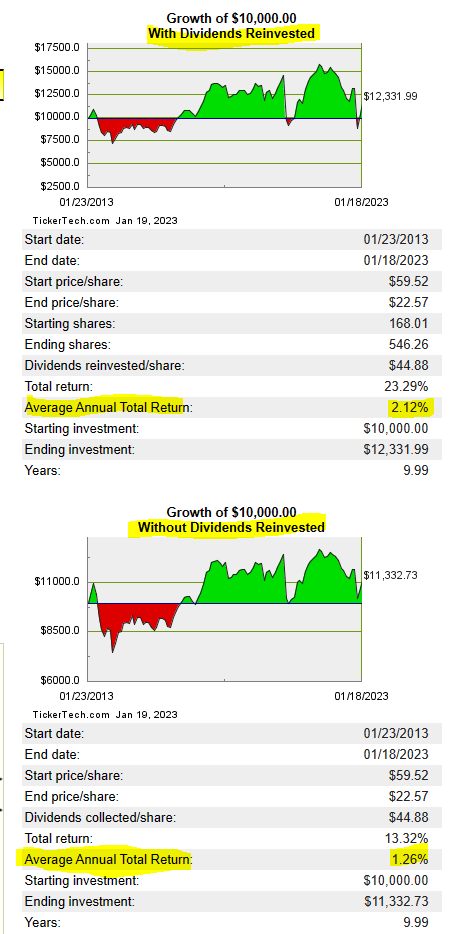

NLY, believe it or not, has actually done worse than the index over the last decade. With dividends reinvested (which is comparable to the mortgage REIT index returns above), NLY did 2.12% over the last 10 years. A shade worse than the 2.37% for the mortgage REIT index.

Split History NLY

With dividends spent, which is how in our experience, 99% of the crowd invests in these, the total returns were 1.26% per annum.

You started with a price of $59.52 (split adjusted) and ended with $22.57. You did get $44.88 of dividends but you lost out $36.95 in price.

10 years back your yield on cost was about 10.4%.

Split History NLY

Today your yield on original cost has dropped to 5.9%. We will bet it will be a lot lower when 2023 is done.

Verdict

Our history on NLY can be easily seen with the snapshot below. We had one sell rating and four hold ratings on the stock in the past 12 months.

Split History NLY

Today we think the climate favors yet another Sell rating and we don’t believe we will see positive total returns over the next 12 months.

The preferred shares of NLY are a different matter. NLY has three preferred share classes outstanding currently.

1) Annaly Capital Management, Inc. 6.95% PFD SER F (NYSE:NLY.PF).

2) Annaly Capital Management, Inc. 6.50% PFD SER G (NYSE:NLY.PG)

3) Annaly Capital Management, Inc. 6.75% PFD SER I (NYSE:NLY.PI)

NLY.PF just moved to floating and is at LIBOR + 4.993%. That should put the yield to close to 10% and that is another big expense for NLY before common dividend coverage begins. We will note that we still don’t have a single quarter where this expense has actually shown up on the statement.

NLY.PG is now two months away from floating at LIBOR +4.172%. Both issues will cost NLY far more on the floating rate than they did when they were fixed. We don’t own any of the preferreds either, as we just don’t like the common equity to preferred equity ratios in these companies. But they all are far better options than the common. If you had held the preferred shares over the last decade, you would have made close to 7% a year in total returns, with far less risk than the common shares making about 2%. Anyone interested in NLY should look closely at these.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment