akinbostanci

Introduction

Where would you invest $10,000 right now? It’s a question I’m often asked, although the number varies from everything between $500 to $100,000. There are a million answers to this question, and the fact that I cover multiple dividend stocks per week is based on answering questions like these. However, in this article, I will give you three stocks I would buy in a heartbeat if I were an investor starting a portfolio or looking for new investment ideas. As we can pick from countless investments, I decided to base this article on a few things:

- Outperforming total returns (otherwise, we might as well buy an ETF).

- Subdued volatility (after all, we want to sleep well at night).

- A satisfying dividend yield (we want income, that’s why we buy dividends).

- Consistent inflation-beating dividend growth.

Hence, I went with actual dividend kings. Stocks that have raised their dividend for at least 50 consecutive years. I picked three stocks that, despite their mature age, will (more than likely) deliver exactly what we need.

So, without further ado, let’s dive in, starting with a bit of theoretical background.

Dividends Make So Much Sense

A dividend aristocrat is a stock that has raised its dividend for 25 consecutive years. That’s impressive, as companies need to remain profitable on a long-term basis and consistently grow their business.

Once companies achieve this, they can eventually become dividend kings, which are companies that have raised their dividends for 50 consecutive years. Fewer than 50 stocks are part of that exclusive club.

These companies were able to remain profitable and grow their business through countless business cycles, dealing with new competitors, disrupting technologies, geopolitical changes, and so much more.

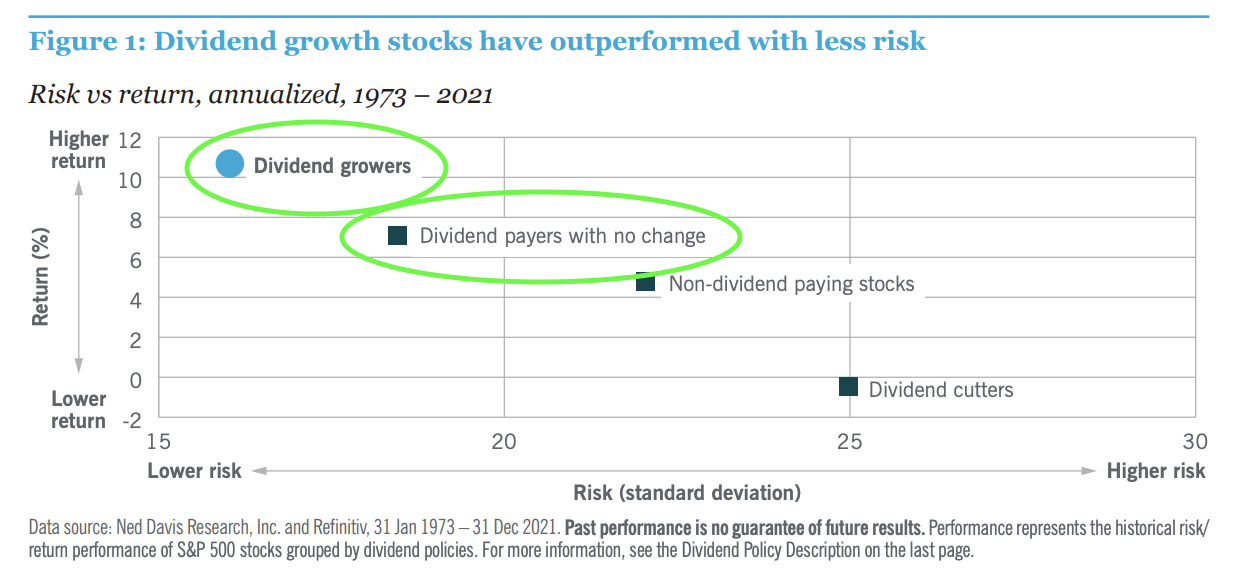

One of the things I have mentioned in almost every single dividend-focused article is the fact that the major benefit that comes with dividend investing is the quality aspect. Because dividend stocks bring something to the table that other stocks cannot compete with (steady cash flows), they tend to do better during bear markets when investors prefer to sell assets with higher risks. So, even if dividend stocks do not outperform in every bull market, downside protection is often enough to provide investors with long-term, low-volatility outperformance.

Nuveen (Author Annotations)

Moreover, S&P Global wrote an interesting paper in 2021, which highlighted some of the other benefits that come with investing in reliable dividends. The paper focused on aristocrats.

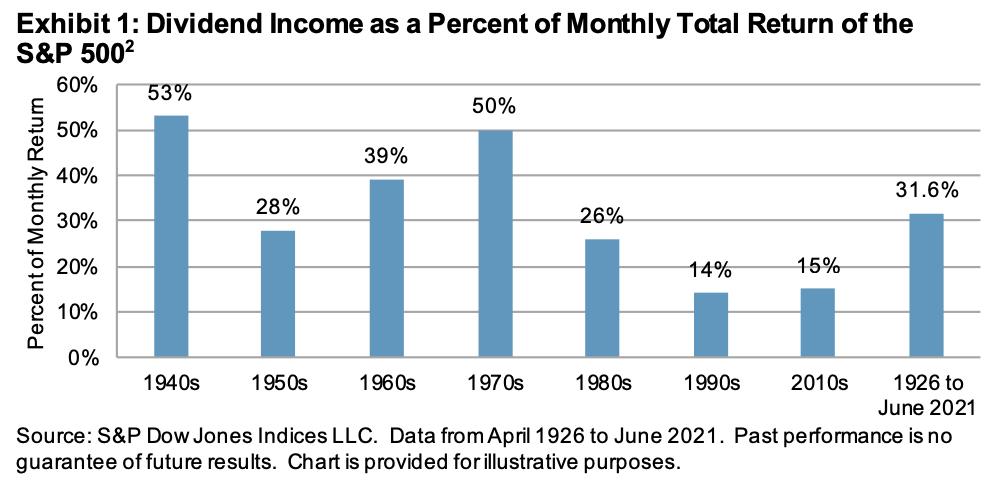

- Dividends contribute 32% of the long-term total return from equity.

Between 1926 and 2021, dividends have contributed 32% of the monthly total return of the S&P 500. The remaining part came from capital returns (stocks going up).

As the fascinating chart below shows, in some periods, dividend returns were much higher. In the 1970s, half of the total returns came from dividends. The same happened during the 1940s.

S&P Global

In the 1970s, dividends were so important because the economy (not just in the US) was hit by high inflation and a central bank failing to contain inflation. They did succeed now and then, but inflation always bounced back. It was a truly horrible situation of long-term above-average inflation.

The same is happening now. Hence, as I wrote in several articles (like this one), I believe that we’re in a new economic regime. I think inflation will remain above average on a prolonged basis, shifting the focus a bit from capital gains to dividend returns when it comes to the bigger (total return) picture.

Oaktree Capital

Now, onto reason number two.

- The compounding effects of dividend income are huge

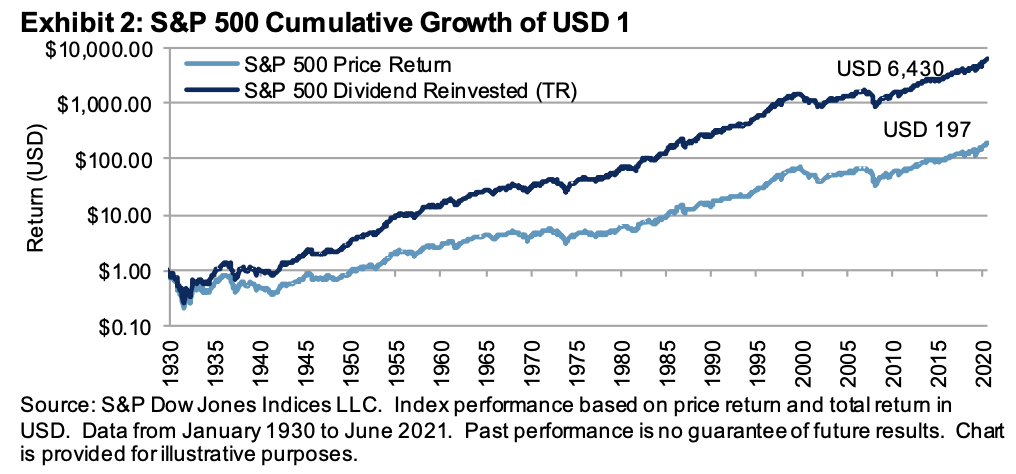

Excluding dividends, a $1 investment made in the S&P 500 in 1930 would have grown to $197 by the end of 2021. Including dividends, that number would have been $6,430.

S&P Global

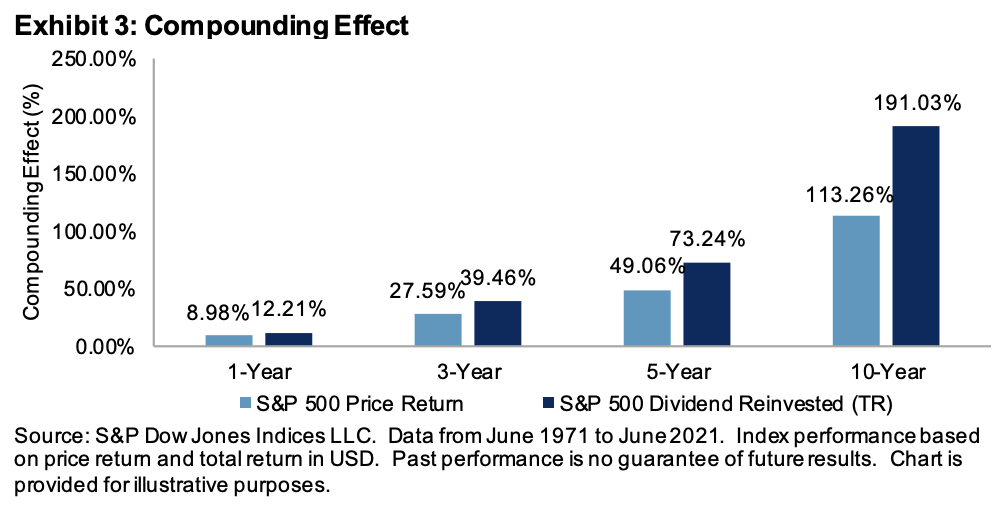

According to S&P Global calculations, the annualized difference between the price return and the total return of the S&P 500 over every 10-year horizon, on average, amounts to nearly 78%. That’s a huge number. As our example just showed, the benefit of dividends grows exponentially over time.

S&P Global

With that said, there are two more things I need to mention.

A Quick Note Regarding The Average Yield & Dividend Scorecards

But first, a quick note before we start. As we already discussed, dividend kings are very mature businesses. A lot of them have very low growth rates. There’s nothing wrong with that. I just prefer to combine dividends and dividend growth.

Hence, in this article, I present three stocks that come with decent yields, solid dividend growth, and all other benefits that come with buying trusted dividend kings.

The ProShares S&P 500 Dividend Aristocrats ETF (NOBL) (I’m using this one as a benchmark for this purpose) yields 1.9%. The average yield of the stocks in this portfolio is 2.2%. The S&P 500 yields 1.7%.

In other words, I’m explaining the benefits that come with buying stocks that are not offering a high yield.

Moreover, I usually use dividend scorecards to give investors a brief overview of the different factor grades. In this article, I’m only doing this once. While it may look like I’m hiding something, I’m only doing it because sometimes I disagree with grades. Because factor grades are automated, data outliers sometimes cause faulty grades. That’s why I don’t always use automated data.

That said, let’s discuss some stocks!

1. Lowe’s Companies (LOW) – 2.1% Yield

59 years of consecutive dividend growth

Lowe’s is one of the few companies that’s old, a dividend king, and still capable of reporting high (dividend) growth rates.

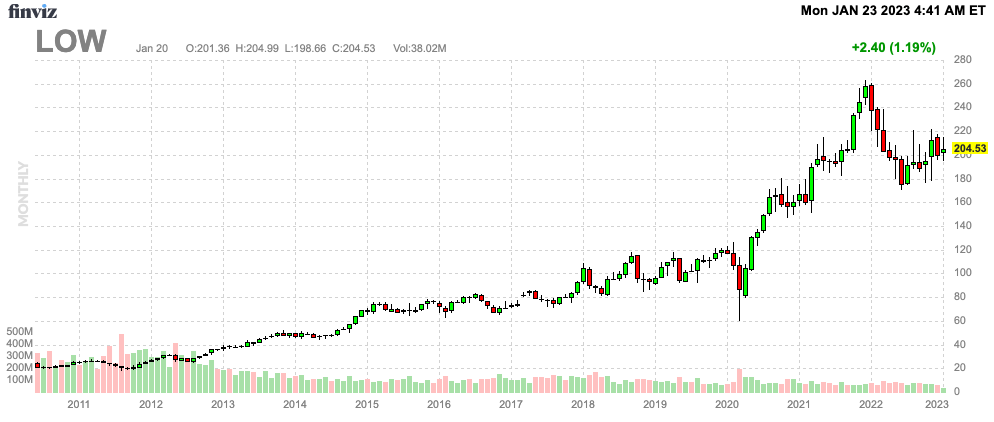

FINVIZ

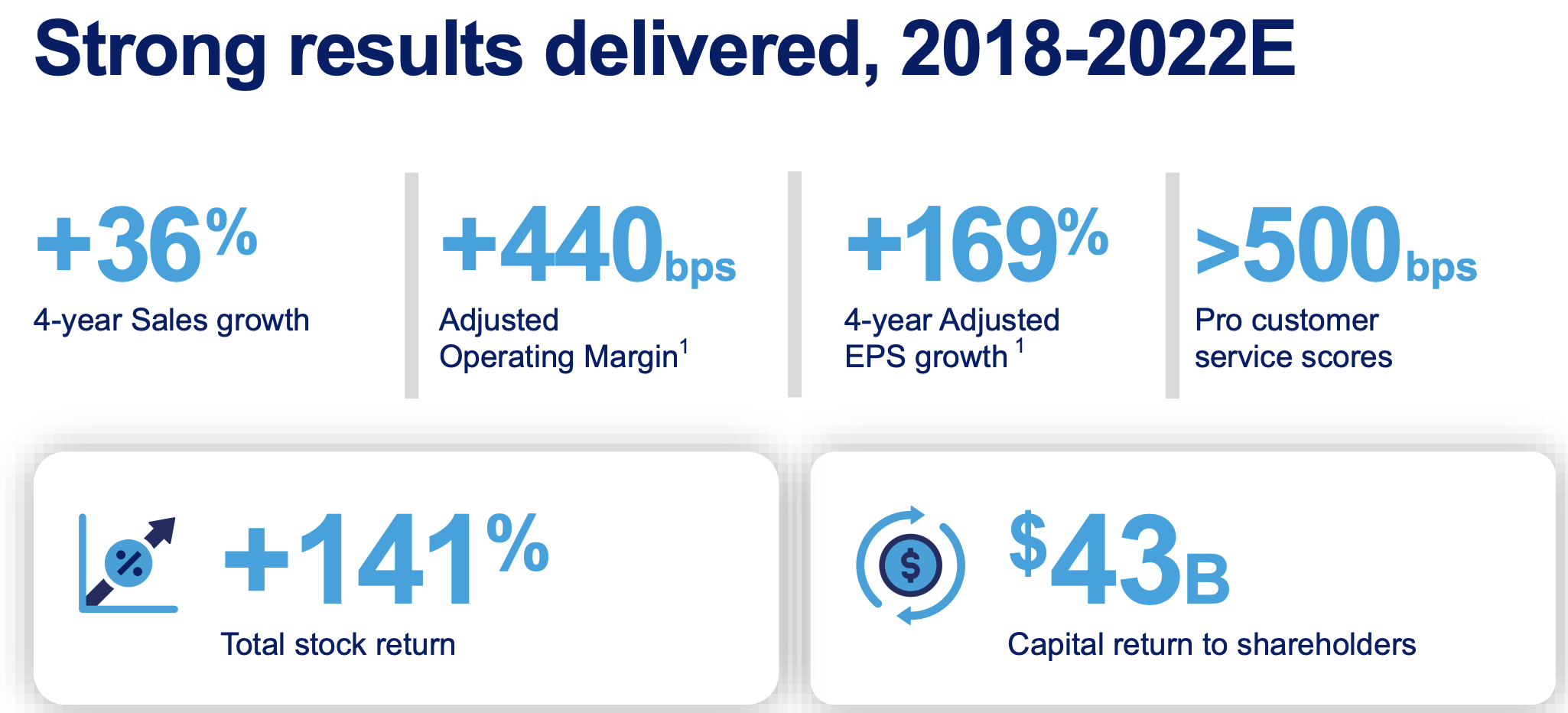

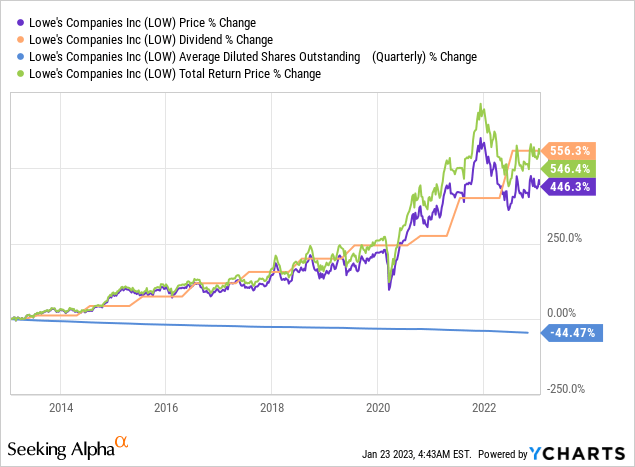

This North Carolina-based home improvement retailer with a market cap of more than $120 billion has rewarded investors with both steady and high dividend hikes and high share buyback programs for decades.

Lowe’s Companies

Over the past ten years, Lowe’s has:

- Bought back 44% of its shares.

- Hiked its dividend by 556%.

- Provided 446% in capital returns.

- Outperformed the market with a 546% total return (dividend impact on capital gains).

These are the historical dividend growth rates:

- 10Y CAGR: 20.0%

- 5Y CAGR: 19.5%

- 3Y CAGR: 21.6%

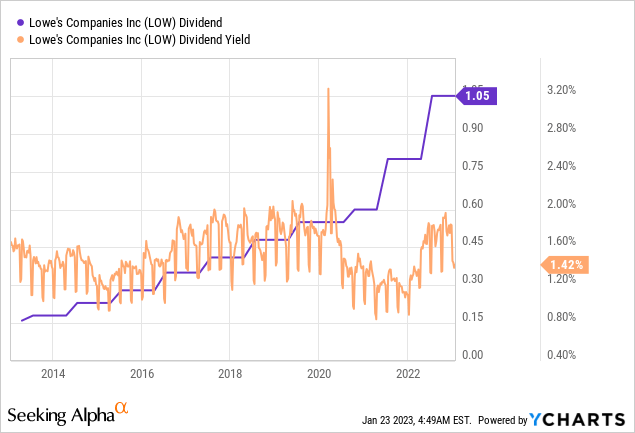

The most recent hike was announced on May 27, 2022, when management hiked by 31.3%.

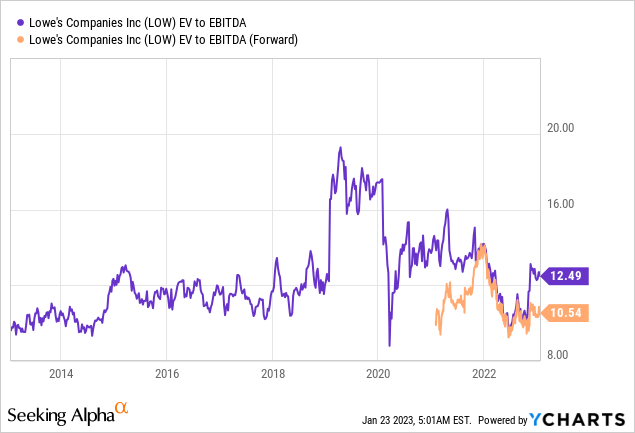

Please note that the yield in the chart below is not up-to-date. LOW yields 2.1%, which is well above the longer-term average, as a result of recent stock price weakness.

Moreover, despite these aggressive hikes, dividend safety remains very high. LOW has an adjusted dividend payout rate of 28%, which is in line with the sector median of 28%. The cash flow payout ratio is 22%, which is one point below the sector median.

At the end of this year, LOW is expected to end up with $29.6 billion in net debt. That is 2.0x EBITDA. The balance sheet has a BBB+ rating.

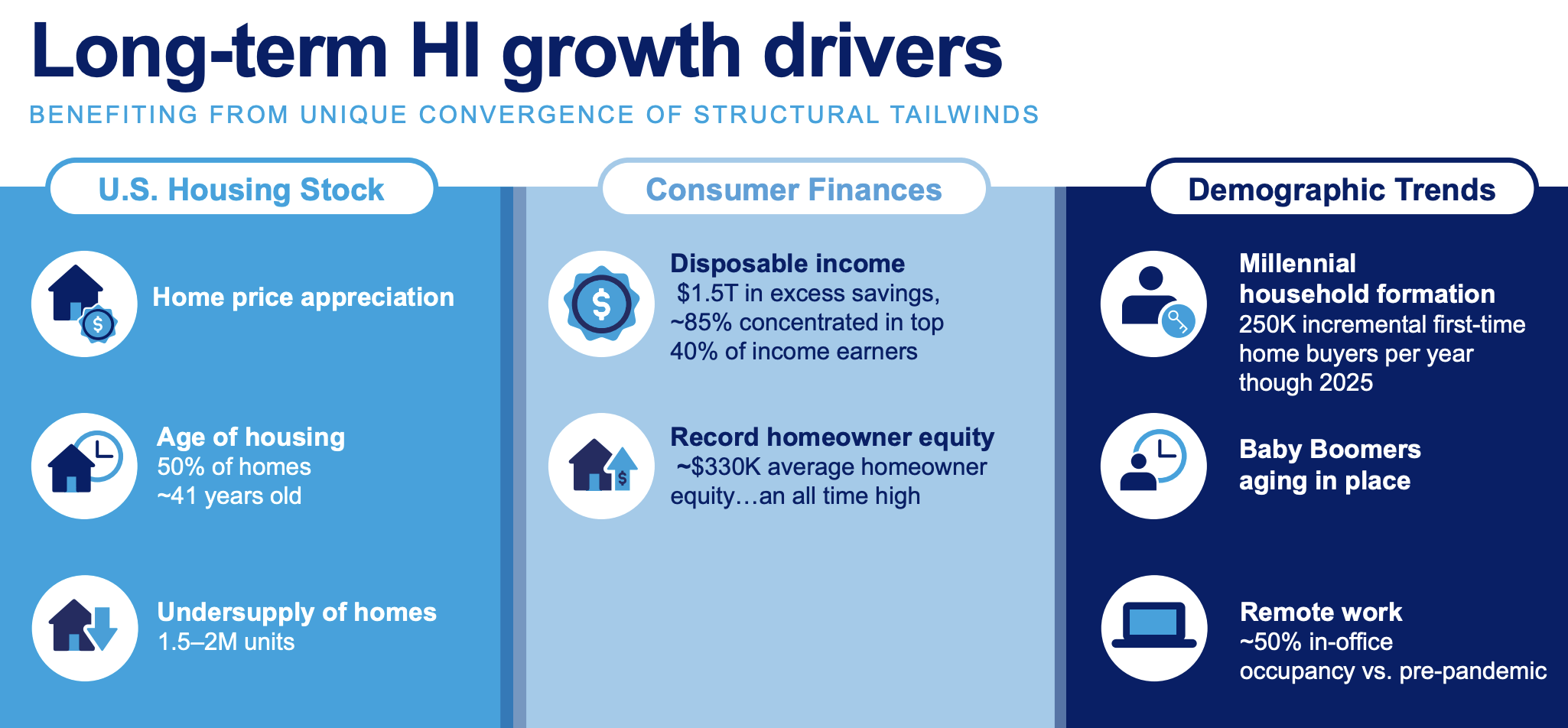

Long-term growth drivers are an undersupplied housing market, a high average home age, increasing homeowner equity, and favorable demographics.

Lowe’s Companies

Unfortunately, the housing market is weakening. Moreover, a toxic mix of an aggressive Fed, persistent inflation, and weakening economic growth let me believe that we might get better buying opportunities in 2023 – despite the current favorable valuation of LOW.

Number two is less cyclical and getting close to a favorable valuation.

2. PepsiCo (PEP) – 2.7% Yield

50 years of consecutive dividend growth

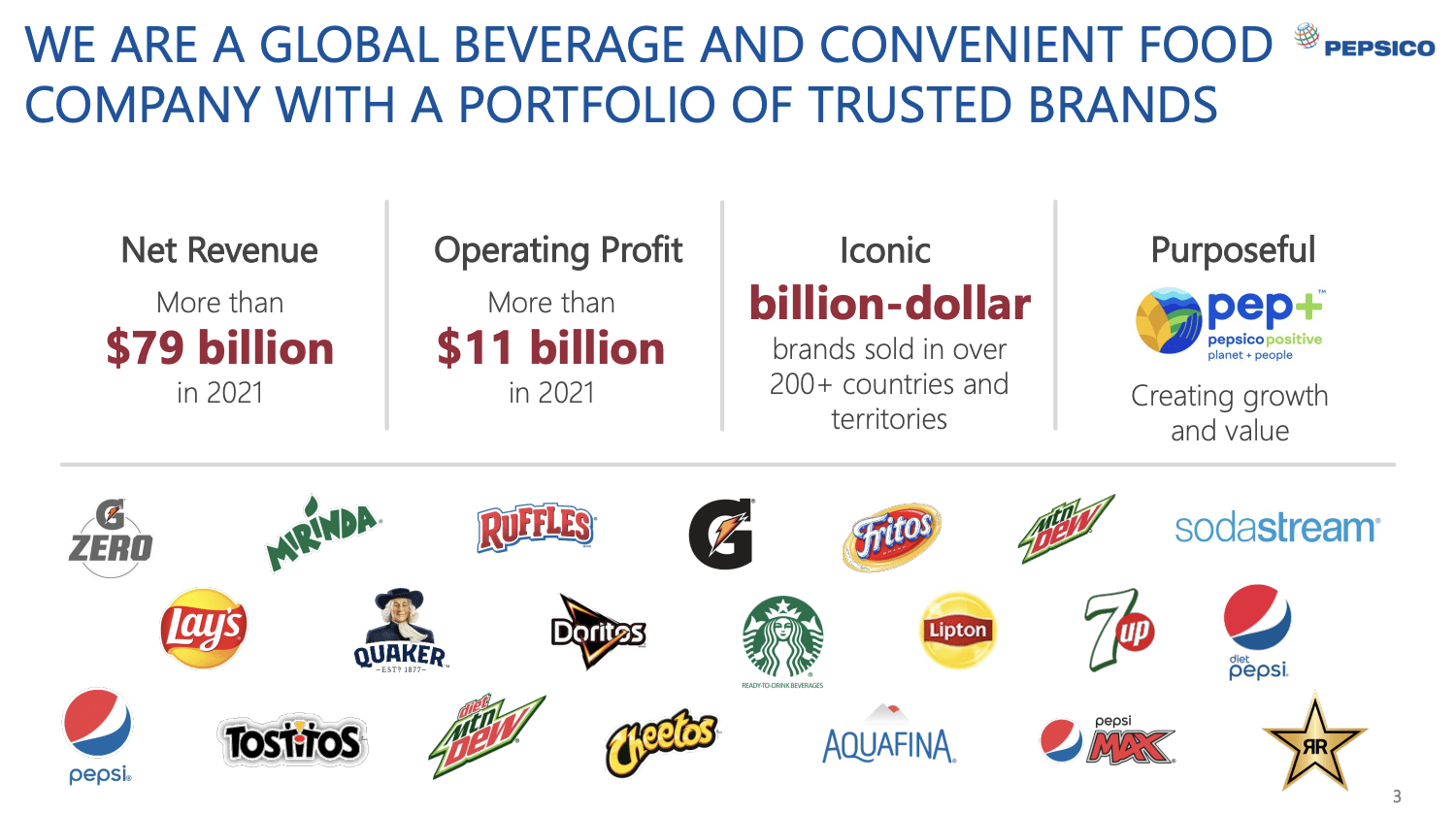

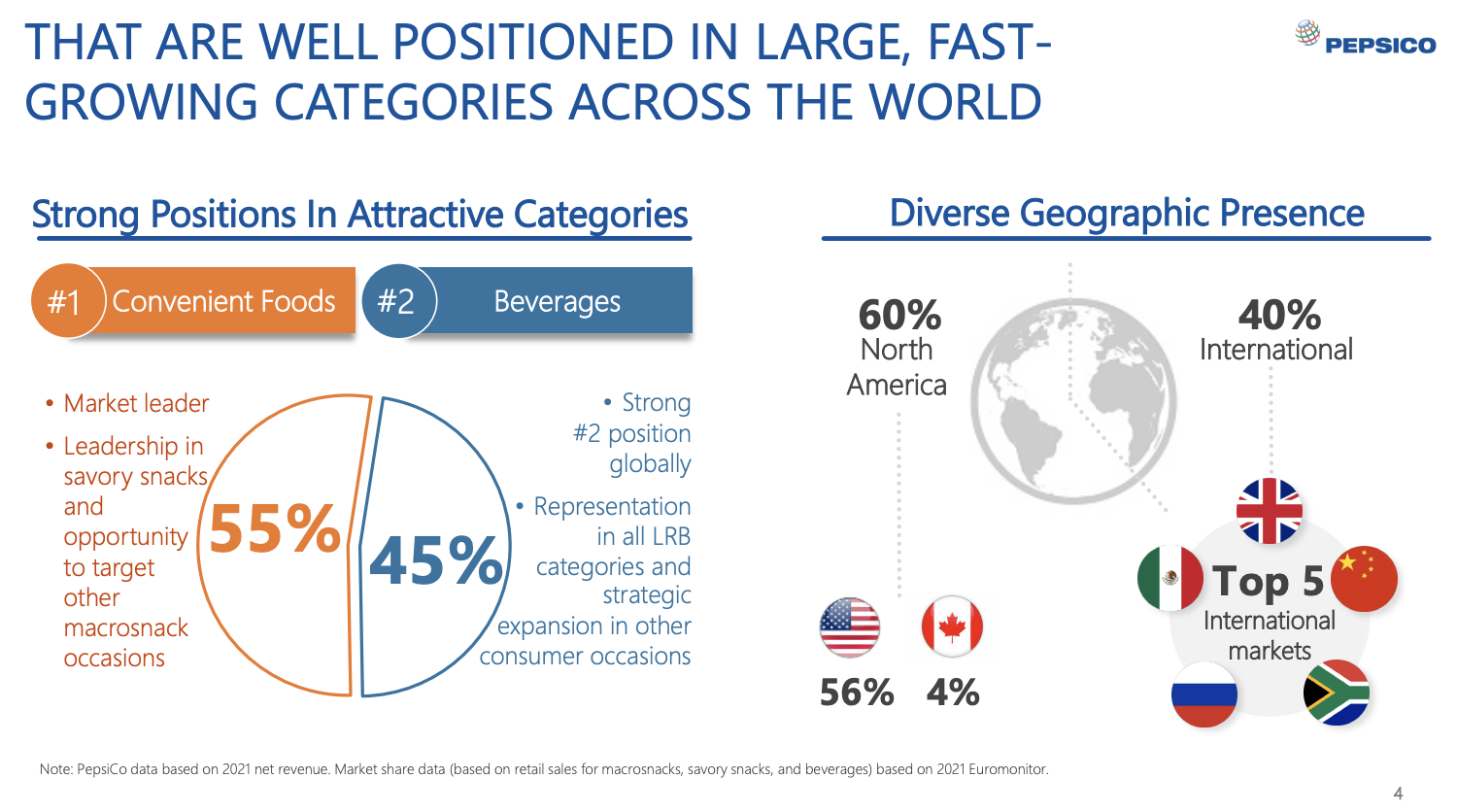

This New York-based consumer staple giant is one of the few companies that doesn’t need an introduction. With more than 20 brands and partnerships, the company dominates the snack aisle in a lot of international supermarkets.

I cannot speak for other nations, but in my country (the Netherlands), PepsiCo more or less owns the entire snack aisle – ignoring generic snacks and brands like Pringles, which PEP does not own.

FINVIZ

The company has grown far beyond its Pepsi brand, offering snacks and beverages in a wide range of categories.

PepsiCo

The company has a wide global footprint and strong pricing power thanks to the aforementioned dominance in convenient foods and beverages.

PepsiCo

In 3Q22, the company reported 16.0% organic revenue growth despite a 1.5% decline in convenience foods volumes and a 3% increase in beverage volumes.

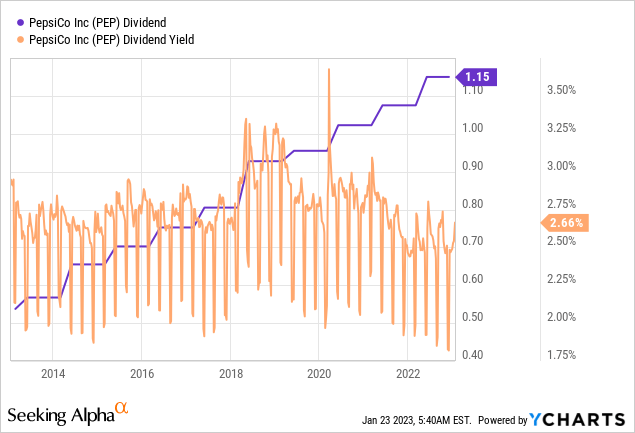

The dividend is backed by a 64% payout ratio, which is a bit elevated but common for mature consumer staples.

These are the historical dividend growth rates:

- 10Y CAGR: 7.8%

- 5Y CAGR: 7.4%

- 3Y CAGR: 6.1%

The most recent hike was announced on May 3, 2022, when management announced a 7.0% hike.

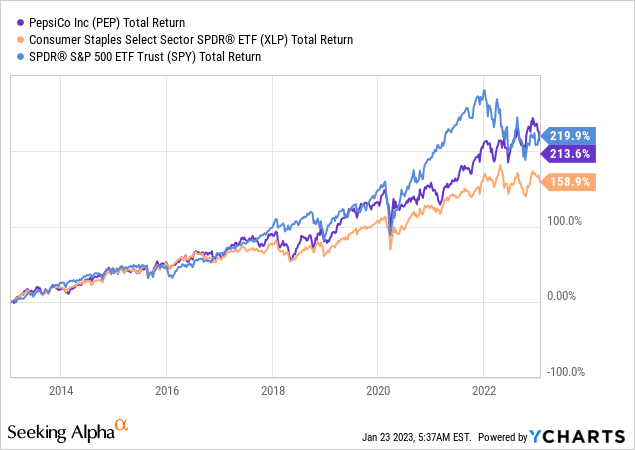

Over the past ten years, the company has returned 214%, which beats the average consumer staple peer by a wide margin. The performance is similar to the performance of the market. Going back further, PEP outperforms the market due to outperformance in bear markets.

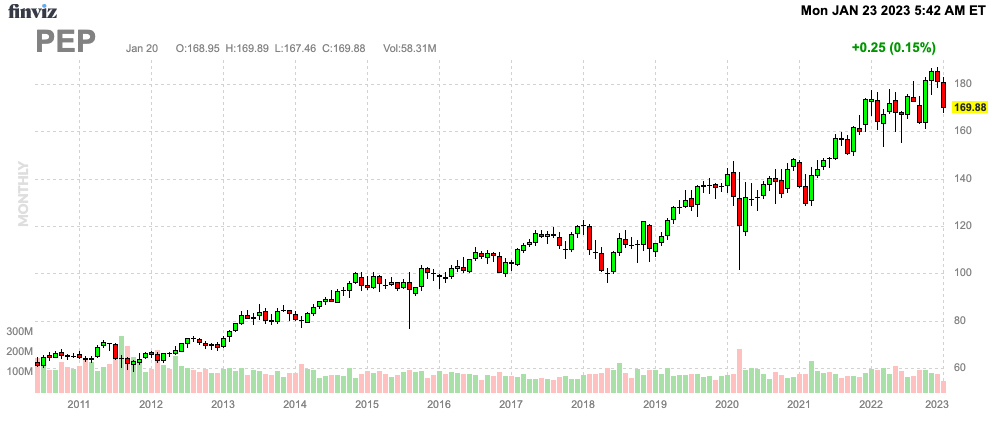

Year-to-date, PEP is down 6% as investors fear that consumer defensives might lose pricing power. After all, inflation looks sticky, and consumer sentiment remains low.

As PepsiCo does have good pricing power, I believe that 2023 will offer new buying opportunities. I will jump in as PEP is now one of my smallest holdings. To boost defensive dividend growth exposure, I will aggressively add to PEP.

Number three is a stock I’ve never discussed, which is a shame as it’s a terrific stock.

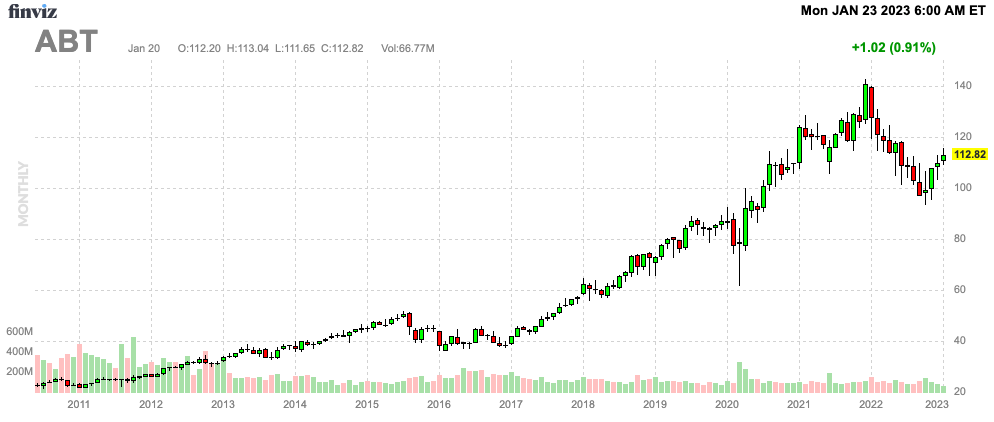

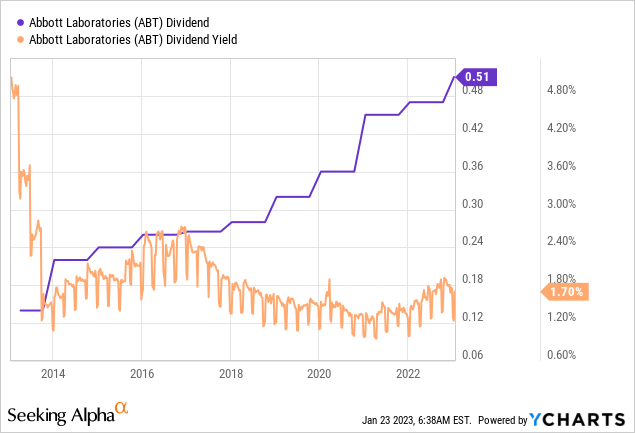

3. Abbott Laboratories (ABT) – 1.8% Yield

50 years of consecutive dividend growth

Multiple websites make the case that Abbott has hiked its dividend for just nine consecutive years. This is the result of a spin-off. In 2013, Abbott spun off AbbVie (ABBV) to focus on medical devices, generic drugs, and diagnostics, which impacted the dividend, yet it had no impact on existing shareholders. Hence, ABT remains a dividend king.

FINVIZ

Abbott’s dividend yield of 1.8% isn’t that special. What makes ABT such a great company is the mix of great qualities it brings to the table.

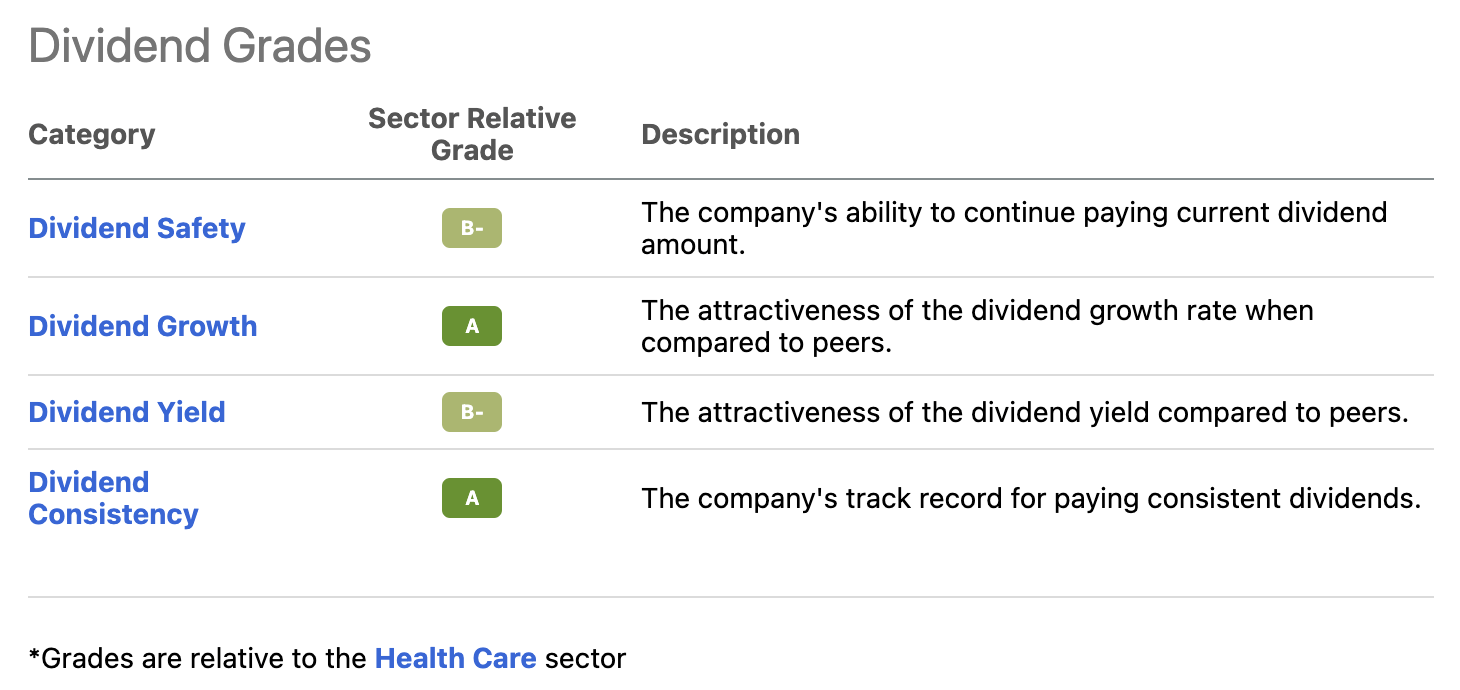

Abbott, which owns a broad line of branded generic pharmaceuticals, diagnostic products, nutritional products, and medical devices, has a very good dividend scorecard.

Seeking Alpha

While ABT has not been a net buyer of its shares in recent years, it has rewarded investors with the following growth rates:

- 10Y CAGR: 8.2%

- 5Y CAGR: 12.3%

- 3Y CAGR: 13.4%

The most recent hike was announced on December 9, 2022, when management hiked by 8.5%.

The dividend payout ratio is 35%, which is attractive. The cash flow payout ratio is just 26%.

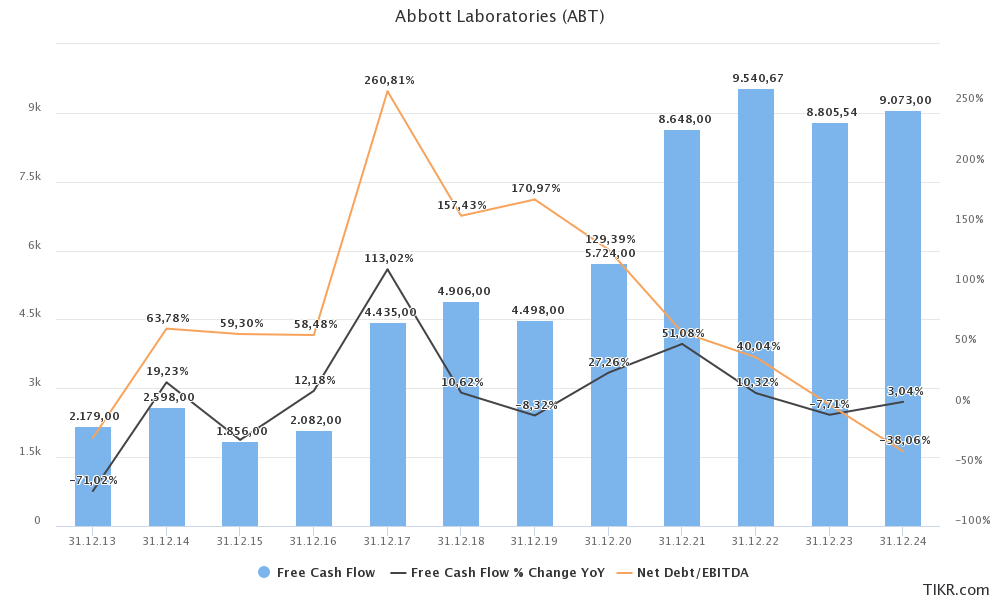

The company has enjoyed strong free cash flow growth. The pandemic helped a lot as it fueled demand for test kits and a lot of other projects. However, free cash flow is expected to grow at moderate rates in the years ahead as pandemic demand fades.

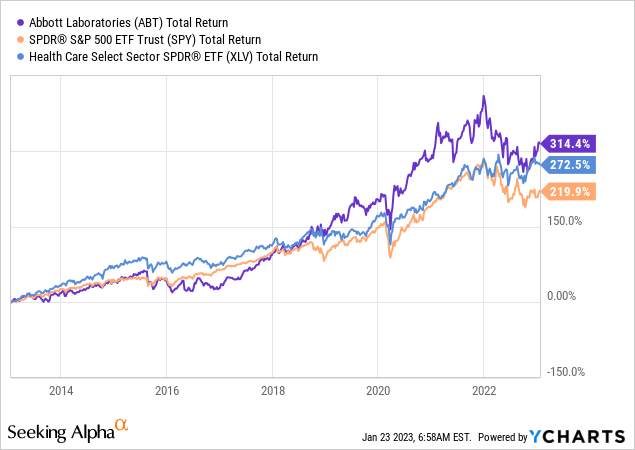

Over the past ten years, Abbott has consistently outperformed its peers and the market.

Also note that the company is about to become net cash positive, meaning it will have more cash than gross debt on its balance sheet. This opens up new opportunities for shareholder distributions. The company’s credit has an AA- rating, which is better than a lot of developed nations.

TIKR.com

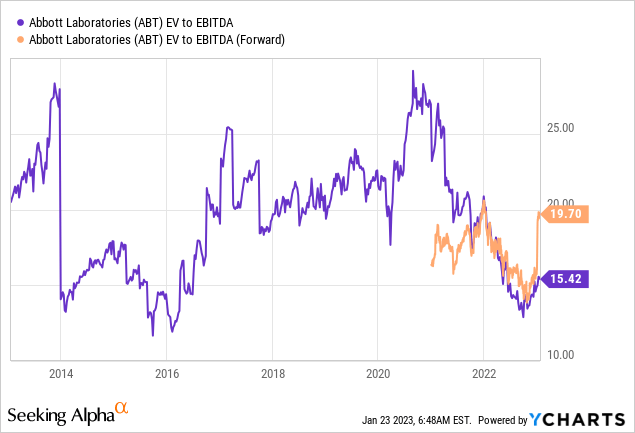

The valuation is very fair. Please note that the forward EV/EBITDA ratio is at almost 20 due to an expected decline of 16% this year. In 2024, EBITDA is expected to pick up again with a growth rate of at least 10%.

I believe that ABT shares are a great addition to dividend portfolios on weakness, especially for investors looking for defensive exposure capable of beating the market on a long-term basis.

One More Chart And One More Table

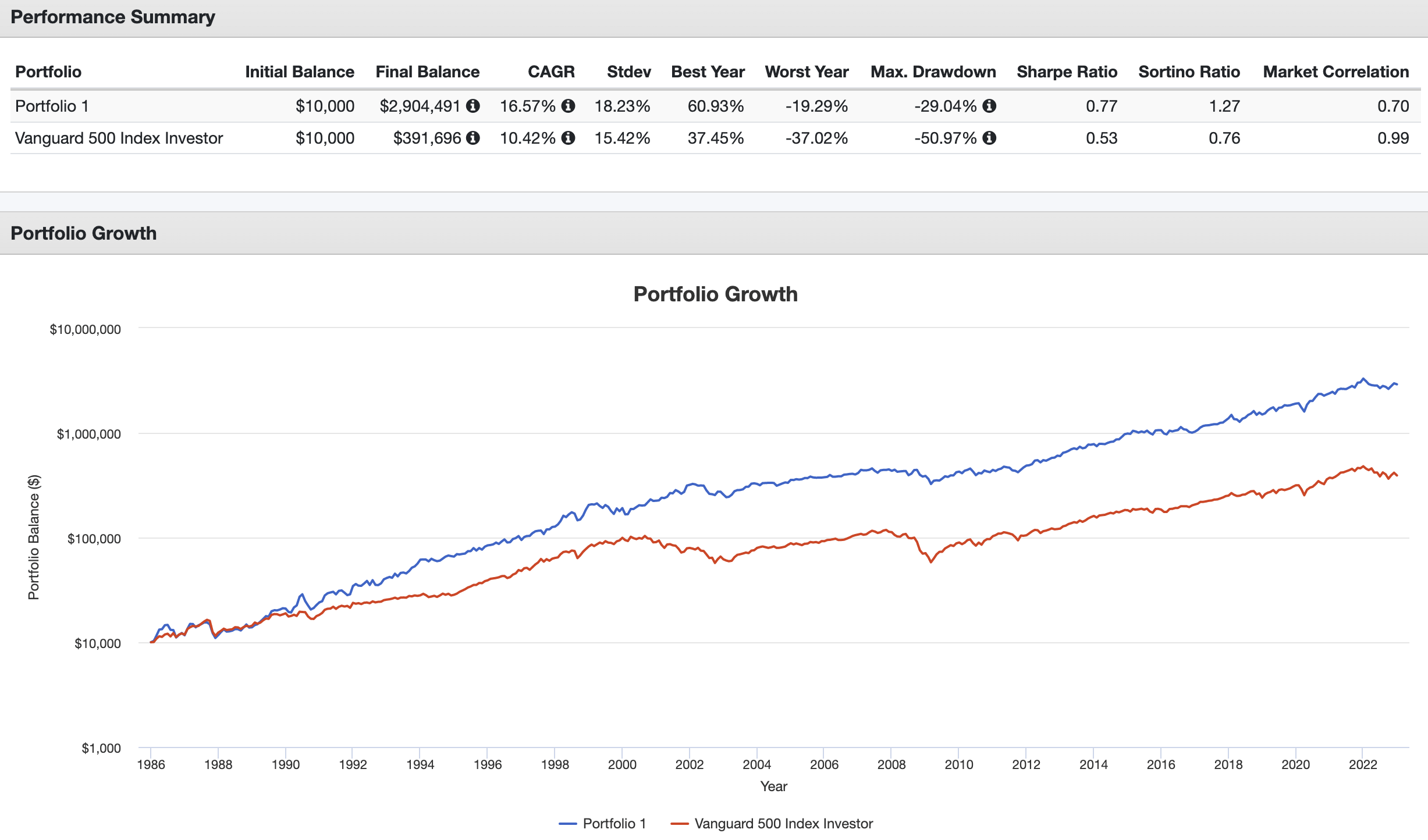

To confirm the power of buying stocks like the ones in this article, I combined all of them in a portfolio, which I backtested. Going back to 1986, an equal-weight portfolio of LOW, PEP, and ABT has returned 16.6% per year, turning $10,000 into $2.9 million. Moreover, the standard deviation of 18.2% is low as it is barely higher than the 15.4% standard deviation of the market. Bear in mind we’re comparing three stocks to a basket of 500 stocks.

Portfolio Visualizer

Even downside protection follows the theories we discussed. The worst year had a drawdown of 19.3%. The biggest drawdown the portfolio experienced was -29%, which is 30 points better than the market.

I’m not making the case that a three-stock portfolio makes sense. I just had to add this to confirm what we discussed in the first half of this article and to highlight the power of conservative dividend growth.

Takeaway

I started this article by discussing the benefits that come with buying trusted dividend stocks. Dividends have been the backbone of wealth generation thanks to consistently growing income, reinvestment benefits, and downside protection.

Hence, I presented three stocks that I like a lot. In this case, the theme was dividend kings. I picked three of my favorites that come with decent yields, satisfying dividend growth, and business models that are likely to provide investors with long-term outperformance in the future.

I believe that all of them are great additions to any dividend portfolio.

That said, do you agree or disagree? What would you do differently? Do you own dividend kings? Let us know in the comment section down below!

Be the first to comment