NicoElNino

| It is the time of year that I rail against taxes; I’ll repeat much of what I wrote last year but with updated numbers. |

Taxes

Every year, average American taxpayers work for more than three and a half months for the government (four in high tax states such as my state of Connecticut) without pay. This is more than we spend on food, clothes, and housing combined. So what’s a self-seeking, rational taxpayer to do? Pay what you owe, but arrange your affairs to owe as little as conveniently possible. There are three ways to maximize your family’s after-tax wealth by avoiding overpaying a corrupt and profligate government with your hard-earned money.

Income tax minimization

If the federal government is going to take several months of your labor each year, the least you can do is not add insult to injury by living in a high tax state like I do. My favorites are Wyoming and New Hampshire. But my favorite US tax jurisdiction is Puerto Rico. And if you want to go all the way to expatriating (or at least have a second passport ready so that you can take that step quickly in a pinch), I like Dominica.

Death and taxes

If you love your kids more than the IRS, you want to make sure that you die with less than $12.06 million to avoid getting slammed with an estate tax (on money that was already taxed once when you earned it and taxed again when it is invested). Maxing out their 529s is a start, which gets you to $500,000 per kid. I want to push as much compounding down generationally. To that end, the annual gift tax exemption is $32,000 per couple to each kid. One could gift that to allow them to build up savings. Better yet, loan them the capital to invest. The current mid-term annual applicable federal rate is 4.27%, so make a rolling loan to each kid and gift the interest payments due to you. By that means you can lend up to three quarters of a million dollars per kid for them to invest (down from over $9 million a year ago).

Loss harvesting opportunities

A third way to avoid the tax man is to dump shares in your losers before year end to lower your capital gains taxes. There’s a time and a place for this. But I prefer to find opportunities to buy other people’s losers when they’ve been pushed to prices far beneath their value. Something always on my mind is the question, “why are sellers selling something to me?” In this case, I have a great counterparty – someone who simply wants a tax benefit. We might actually both add to our after-tax wealth if he gets the tax benefit and I get the bargain. So if over the course of this month you see this year’s losers plunge further, you might want to scoop some of them up. 2022’s losers could be among 2023’s biggest winners. My favorite: BankFinancial (NASDAQ:BFIN).

Value?

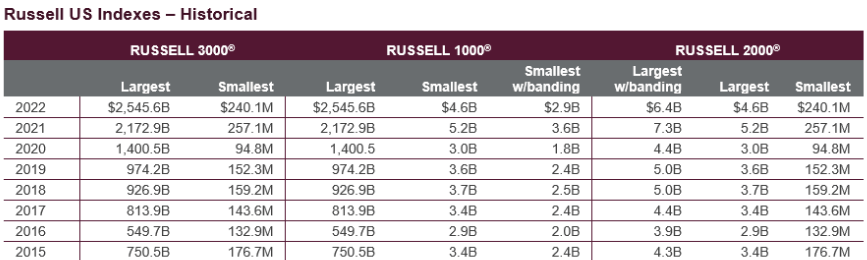

BankFinancial converted from a mutual to a stock in 2005. It costs 79% of tangible book value and 8x achievable 2023 earnings estimates. The stock has gotten hit with index sell imbalances combined with tax loss selling. It’s in the Russell Microcap Index. The big sell imbalance day was last Friday when it traded almost a hundred thousand share (a lot for this sleepy little stock) and had a big market on close imbalance. The fact that the bank bought back so much stock back reduced the share count, and thus reduced the weighting in the index. The CSRP Index rebalance also took place over the past week which further exacerbated tax loss selling. Specifics are hard to glean since those indexes don’t disclose the weightings. BFIN is around a $120 million market cap, so it could easily catch the Russell vacuum in the next reconstitution (the cutoff will decline due to no IPOs but mergers still closing and the SPAC world dying). The 2020 cutoff was about $95 million, 2021 was $257, 2022 was $240, and analysts have estimated the next one to be $183 million. To be determined if BFIN makes it, but it is entirely possible.

Russell

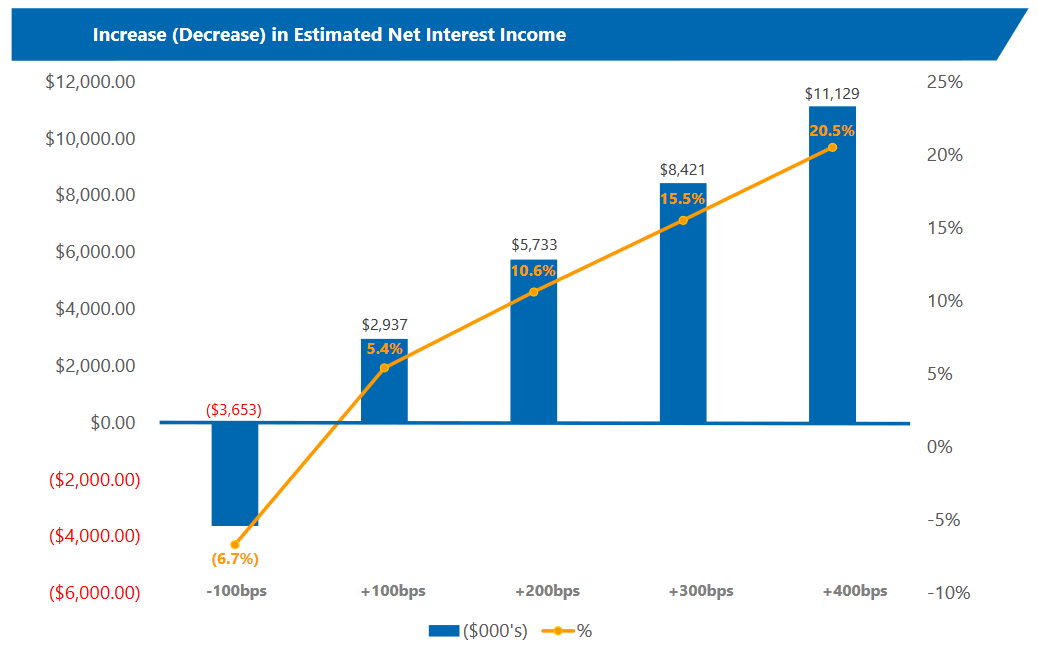

Their balance sheet is perfectly positioned for rising interest rates with a ton of cash going into the rate hikes and only a tiny securities portfolio. At the end of last year, they had nearly 30% of the balance sheet sitting in cash as they weren’t willing to deploy deposits into low-yielding assets like many other banks. That proved wise. Earnings suffered given their conservative posturing, but as rates rose, they gradually deployed that cash into higher yielding assets. They now have $162 million of short-term Treasuries (95% under three-year maturities) and cash is down to 13% of assets as they have moved the cash into higher yielding loans and the Treasuries. This savvy timing increased the yield on their assets and is why earnings in 2023 are expected to be 43% higher than in 2022, and 115% higher than they were in 2021.

They aggressively bought back stock since converting and have retired almost half of the issued shares. As is all too common, they botched the timing and paid a much higher average price than shares cost today. Last year their average per share was $11.09 for 1,541,280 shares, 2020 was 508,699 shares at $9.04, but in 2019 they bought 1,203,050 shares at $15.05. It pays out a 4.3% dividend. Even if nothing much happens, this one is probably pretty safe at a single digit price. Underpay, clip a divvy, and wait.

BFIN

Catalyst?

BankFinancial deserves a scarcity premium. There aren’t many community banks over $1 billion in assets in Chicago and this one has a very valuable deposit franchise. It’s a cinch to find strategic buyer interest… but will management sell? The CEO is just 58-years-old (which sounds younger and younger to me each year), which is typically a negative in an M&A target. He may want to work for many years. At the same time, he’s also the largest shareholder with 307,529 shares and a change of control agreement worth $1.73 million, so he could sell and walk away with millions of dollars. His decision to accept under-earning for the past five years due to a conservative balance sheet would have led to a lowball M&A price. But now that the bank’s earnings power has been unlocked, he can get a full price. He went through a mutual to stock conversion to make money. He’s a capitalist. He’s there to monetize this investment and 2023 is the optimal year to do it.

BFIN

Conclusion

Pay the government what you owe but not $0.01 more. Live in Wyoming, New Hampshire, or Puerto Rico. Lend your kids all that you can for them to invest. And be a service provider to investors dumping their losers at year end for tax losses: Buy what they are selling when they sell too cheaply.

Buy BFIN for under $10 in December 2022. It’s worth around $12 (approximately its tangible book value) by January 2023 and around $15 per share to BFIN holders in a sale for 125% of that TBV by January 2024. Not that the target’s holders will realize the full value (the buyer will want something for the price that they pay) but the franchise value could be worth as much as $20 per share. It could continue to wilt between now and New Year’s Eve on further tax loss selling pressure but could bounce back hard in the New Year.

BFIN

TL; DR

Buy BFIN, a bank that benefits from rate hikes:

BFIN

Be the first to comment