Denis_Vermenko

Some investors like to wait for capital gains. However, in this tumultuous market, capital gains can be fleeting, as what shareholders saw with Google (GOOG) and Amazon (AMZN) in recent weeks. Heck, even Air Products and Chemicals (APD) saw a material price drop after its earnings release.

That’s why it may be a good idea to have healthy exposure to big dividend payers that pay you real cash now, with which you can treat you and your loved ones to a fancy dinner or a vacation.

This brings me to the following 2 picks, both of which throw off high yields that may benefit income investors in both the near-term and/or the long-run, should one so choose to reinvest into the same or other income producing assets.

Pick #1: Verizon

Verizon (VZ) admittedly has been a battleground stock for the better part of the past several months, due to underwhelming growth and heightened competition from peers AT&T (T) and T-Mobile (TMUS). However, there’s no denying its moat-worthy telecom asset base, which serves over 90 million postpaid and over 20 million prepaid customers.

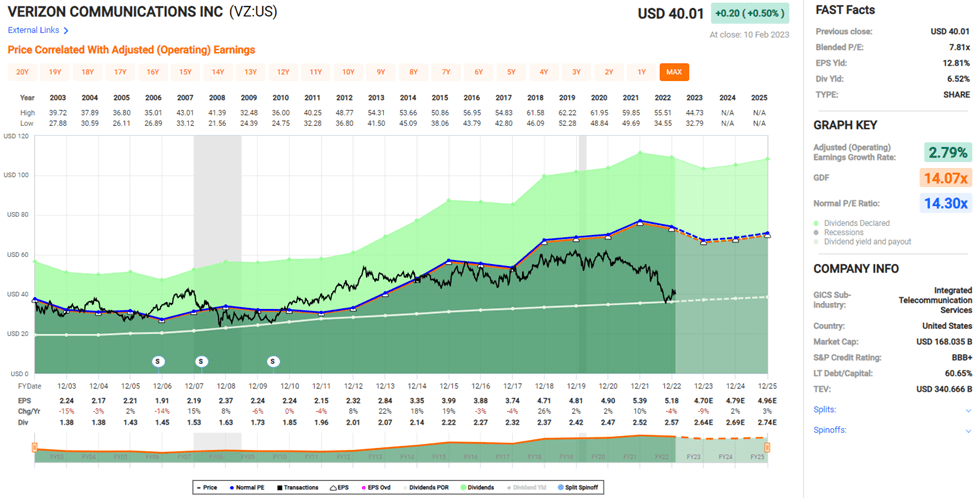

Despite the gloomy sentiment surrounding the stock, Verizon is actually delivering results that aren’t bad. This includes consolidated revenue being up by 3.5% YoY to $35 billion during the fourth quarter.

This was driven in large part by wireless service revenue growth of 6% YoY, benefitting from the best fourth quarter total postpaid net additions in seven years, positive pricing actions, and a full quarter’s contribution from Tracfone, the prepaid phone service that Verizon acquired.

It’s worth noting, however, that Verizon isn’t immune to inflationary pressures, as this combined with higher promotional spend resulted in adjusted EBITDA being down by 0.2% during the fourth quarter.

Nonetheless, Verizon continues to be a cash flow generating machine, delivering $14.1 billion of free cash flow during full year 2022, more than covering VZ’s $10.8 billion in dividends paid last year. Moreover, VZ’s dividend is very well-covered from an earnings perspective at a 50% payout ratio, based on adjusted EPS of $5.18 last year.

Looking forward, home internet evolving, and VZ is in position to benefit through continued expansion of its fixed wireless offerings. Fixed wireless enables VZ to tap 5G capacity to serve residential customers with home internet. Verizon was able to add an impressive 1.3 million broadband subscribers last year. This growth appears to be accelerating, as 416K adds came from Q4 alone.

Meanwhile, VZ continues to maintain a conservatively managed BBB+ rated balance sheet with a net debt to EBITDA ratio of 2.7x, which is reasonable considering the capital requirements of VZ’s 5G buildout.

Turning to valuation, VZ appears to be in deep value territory with a blended PE of 7.8, sitting far below its normal PE of 14.3. While analysts predict low single digit growth over the next couple of years, VZ’s dirt cheap valuation appears to already more than bake that in. Analysts have a conservative price target of $45.75, which could still translate to a potential total return in the high teens over the next 12 months.

FAST Graphs

Pick #2: Starwood Property Trust

Starwood Property Trust (STWD) was founded over 30 years ago, and is led by long-time CEO and Chairman, Barry Sternlicht, who has been in the real estate business for decades. Since its founding, STWD has deployed over $90 billion in capital and, at present, manages a portfolio of $27.5 billion in total assets.

Starwood has proven to be rather resilient and is benefitting from higher interest rates. This is reflected by undepreciated book value growing by $0.18 sequentially in its last reported quarter, to $21.69. It’s also adequately covering its $0.48 dividend with $0.51 in distributable earnings per share.

STWD is also more than just a commercial mortgage REIT, as it has a robust infrastructure lending arm and has equity ownership stakes in properties as well. STWD’s infrastructure lending portfolio is at a sizeable $2.5 billion, and consists of thermal/natural gas (62% of portfolio), and midstream/downstream assets (37%), which are less subject to swings in commodity prices.

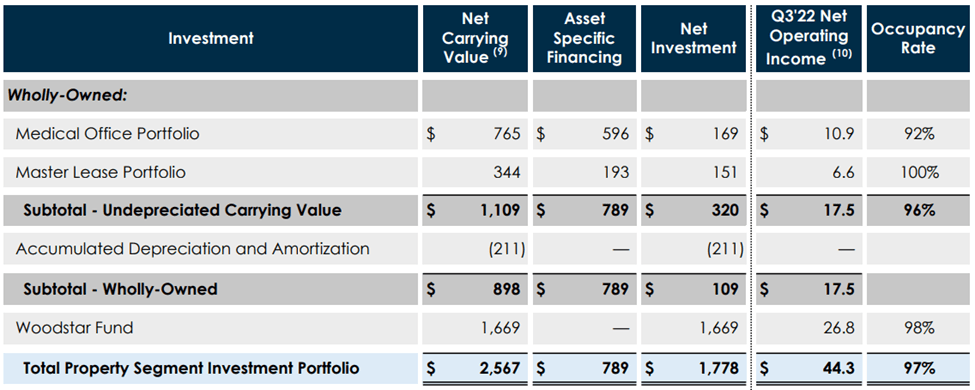

Moreover, STWD’s owned portfolio is comprised of durable assets such as medical office buildings, as well as properties subject to master lease agreements, and its Woodstar Fund, which is comprised of affordable housing units. As shown below, all three asset classes in STWD’s owned portfolio exhibits strong occupancy rates.

Investor Presentation

Looking forward, STWD carries a respectable BB+ rated balance sheet (most commercial mortgage REITs are not investment grade rated), with a debt to equity ratio of 2.4x and $1.3 billion in total liquidity, enabling it to be opportunistic in taking advantage of attractive opportunities should they arise. Notably, management is pivoting towards safer asset classes and away from office properties as collateral, as 46% and 30% of its loan investments in the last reported quarter were multifamily and industrial, respectively, with weighted average 60% loan-to-value ratio.

STWD should also continue to benefit from higher interest rates as 99% and 97% of its commercial and infrastructure debt investments are floating rate, and Fed Chairman Jerome Powell noted earlier this month that interest rates need to keep rising to quash inflation.

Turning to valuation, I find STWD to be attractive at the current price of $20.21 with a price to undepreciated book value of 0.93x, and a 9.5% dividend yield. This could translate to a potential 17% total return over the next 12 months, should STWD return to book value. Meanwhile, analysts have a consensus Buy rating with a more aggressive price target of $24.13, implying that they believe STWD deserves to trade at a premium to its undepreciated book value.

Investor Takeaway

Both Verizon and Starwood Property Trust appear to be undervalued at the current prices, with potential total returns in the high teens over the next 12 months. VZ’s valuation appears to have more than baked in low growth expectations in the near term, while STWD is paying out a juicy 9.5% dividend yield and is positioned to benefit from higher interest rates. As such, both picks offer investors strong current income potential as they navigate a choppy market.

Be the first to comment