monkeybusinessimages/iStock via Getty Images

Co-produced with “Hidden Opportunities.”

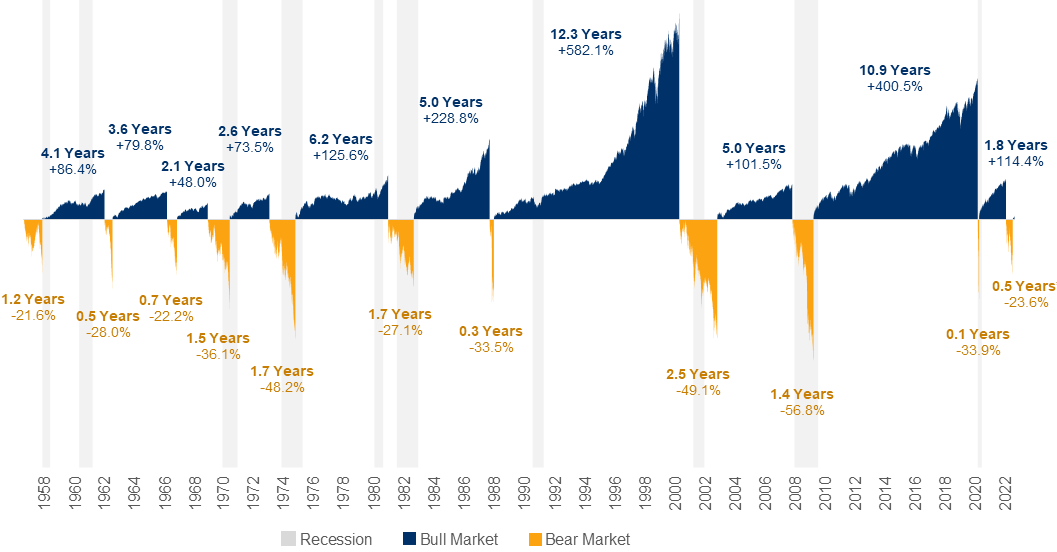

Americans are seeking safety in these uncertain economic conditions. Data from Alight Solutions (a leading administrator of 401(k) plans) shows us that during Q4 2022, investors sold out of target-date funds and large-cap U.S. stock funds in favor of “safer alternatives” such as value, money market, and bond funds.

Retirement savers seem to have been spooked by wild swings in stocks in Q4 after having already suffered significant losses in 2022 amid worries about inflation, interest rates, geopolitical turmoil, and other factors.

Selling stocks out of fear is like making a bad driving decision. If you panic while driving, you’ll get in an accident – Philip Chao, Chief Investment Officer, Experiential Wealth.

No matter the severity of the bear market, investors’ portfolios tend to recover over time. The markets bounce back, stabilize, and set the stage for long-term growth. Staying invested and adding more shares to the portfolio at lower prices are the best course of action. At the end of every dark tunnel is a multi-year bull market with generational wealth-building prospects that you don’t want to miss. Source.

RBC Global Wealth Management

Fixed-income securities provide excellent safety and high yields during chaotic market conditions. Their consistent dividends let you better resist the temptation to sell, and the safety provided by this asset class enables you to be a buyer. The best part is that there is still plenty of quality yield at deeply discounted prices. Two great preferred securities with up to 8% yield to add safety and enable a rich retirement.

Pick #1: HT Preferreds, Yield +7%

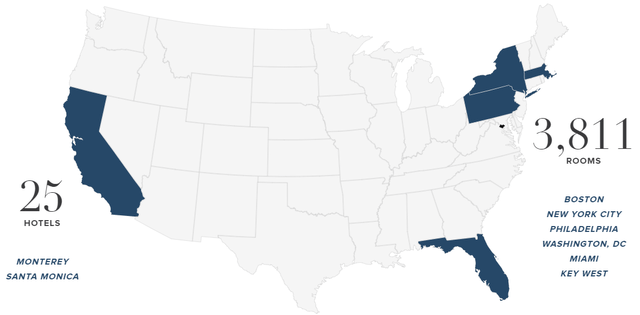

Hersha Hospitality Trust (HT) operates 25 hotels in high barrier-to-entry urban gateway markets and resort destinations.

Hersha.com

In an industry marred by COVID-19 and associated travel restrictions since 2020, HT has been one of the most impressive turnarounds. Through the chaos, management has maintained a substantial stake in the company with opportunistic additions through their journey from survival to optimized business functions. Today, HT insiders have 18.2% ownership in the company, including common, preferred, and restricted shares. We like management that eats their cooking and finds additional confidence in the investment, knowing that the interests of all parties are aligned.

HT has been pursuing the sale of non-core properties in urban locations and generated ~$650 Million in gross proceeds from hotel sales. This produced $200 million in gains and management announced a $0.50/share special dividend for common shareholders. In September, HT also announced the resumption of a common dividend that had been suspended since COVID.

I am very pleased to announce that our Board of Trustees has approved this significant special dividend as a result of the gains generated from our strategic dispositions. The $650M in sales generated nearly $200M in gains. The proceeds from these sales facilitated a comprehensive refinancing which substantially de-levered our balance sheet and eliminated near-term maturities. The impact of these transformational sales, in conjunction with the cash generation of our portfolio, will lead to $225M in year-end cash holdings. This special dividend, along with the continuation of our common dividend, demonstrates not only the success of our disposition strategy but also our confidence and outlook for our streamlined portfolio. – Jay Shah, CEO.

From the special dividend, we can see that management is committed to enhancing value for shareholders. As income investors, we like the opportunity presented by HT’s discounted preferreds. These are cumulative preferreds; common shareholder happiness is a considerable incentive for our long-term income prospects.

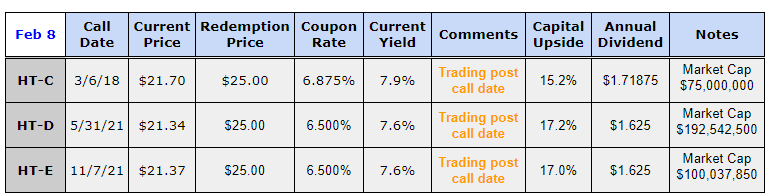

Hersha Hospitality Trust, 6.875% Series C Cumulative Redeemable Perpetual Preferred Shares (HT.PC).

Hersha Hospitality Trust, 6.50% Series D Cumulative Redeemable Perpetual Preferred Shares (HT.PD).

Hersha Hospitality Trust, 6.50% Series E Cumulative Redeemable Perpetual Preferred Shares (HT.PE).

Author’s calculations

HT preferreds trade at a considerable discount to par, positioning patient investors for a sustainable +7% yield and ~16% capital upside upon redemption.

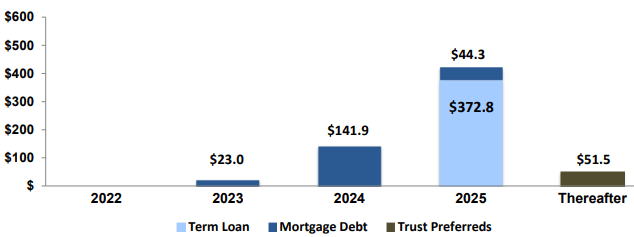

In Q3, HT used the proceeds from the sale of properties to redeem high-interest debt. With these settlements, the real estate investment trust (“REIT”) reported that 71% of their total debt carries fixed rates. Source: January 2023 Investor Presentation.

HT January 2023 Investor Presentation

With no significant debt maturities on the horizon and reduced interest expenses, HT has increased flexibility with its cash flows. YTD, the company spent $18 million on preferred dividends and ~40 million on interest expenses. These are adequately covered by the REIT’s net cash from operating activities ($65.3 million YTD). At the end of Q3 2022, HT spent $8.3 million on common dividends.

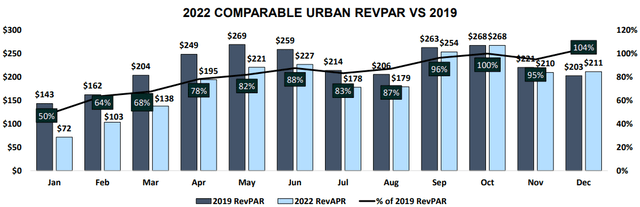

U.S. travel demand has been strong in 2022, and HT demonstrated a healthy 32% EBITDA margin. 60% of HT’s portfolio rooms are located in urban gateway markets, and the company surpassed pre-COVID RevPAR levels (revenue per available room) in December. Management also stated that the REIT’s properties in New York, Boston, and Washington, DC all experienced RevPAR growth in Q4 compared to 2019.

HT January 2023 Investor Presentation

HT’s preferreds present a high-yield investment backed by a closely aligned management team. These deep discounts present attractive buying opportunities for your long-term income needs.

The three HT preferreds are very similar and all are past their call dates. Trading volumes are low and bid/ask spreads tend to be wide, but HT-D usually has more liquidity.

Pick #2: RTL Preferreds, Yield 8%

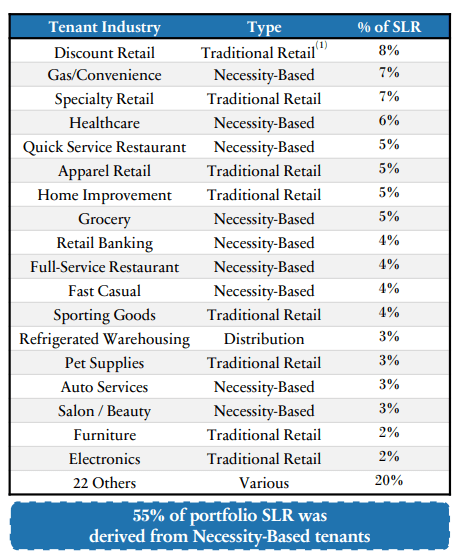

The Necessity Retail REIT, Inc. (RTL) is the landlord of some of America’s leading retailers, where physical presence forms the basis of everyday business. Notably, 55% of RTL’s Straight-Line-Rent (“SLR”) comes from retailers whose operations are necessity-based, service retail, and experiential retail tenants, with adequate insulation from the eCommerce disruption. Source.

RTL November 2022 Investor Presentation

In Q3, RTL’s Adjusted EBITDA was up 14% YoY to $71.7 million, and the REIT’s cash NOI was up 12% to $85 million. Their top 10 tenants represented 28% of the portfolio SLR (down from 38%). The REIT also completed 41 new multi-tenant leases, 42 multi-tenant renewals, and three single-tenant renewals during the quarter. RTL reported an improved portfolio occupancy of 90.6% (up from 87.9% in Q3 2021). The tenant portfolio has a well-balanced lease maturity schedule with a weighted average Remaining Lease Term of 7 years. This positions RTL well for sustained operations and portfolio improvements in the foreseeable future.

RTL maintains a healthy balance sheet with a weighted average interest rate of 4.2%, with 83.1% of debt at fixed interest rates. Notably, 63% of RTL’s debt is set to mature after 2026, giving the company significant flexibility with its cash flows in the near term.

In RTL, we find a strong-performing REIT with a portfolio capable of maintaining occupancy levels through a recession. We see the REIT’s discounted preferreds to be a fantastic bargain at this time.

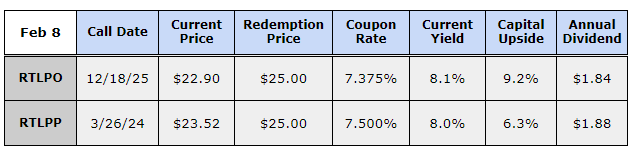

Necessity Retail REIT, 7.375% Series C Cumulative Redeemable Perpetual Preferred Stock (RTLPO).

Necessity Retail REIT, 7.50% Series A Cumulative Redeemable Perpetual Preferred Stock (RTLPP).

Author’s calculations

As of Q3, RTL has spent ~$18 million on preferred dividends and ~$84 million on interest expenses. RTL maintains 2.5x interest coverage. During the nine months of FY 2022, RTL reported an AFFO of $104.3 million, of which $83.6 million was used toward common stock dividends. The preferred dividends have adequate coverage and present a safe income opportunity.

With a discount to NAV and an 8% yield, when markets are fearful, we should be greedy and lock in high yields and capital upside to par value.

Shutterstock

Conclusion

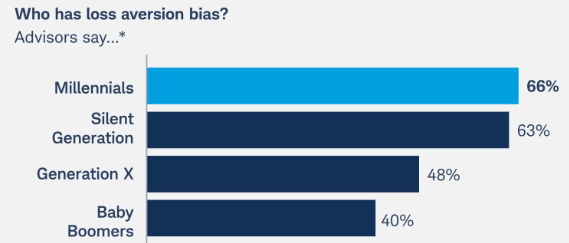

Loss aversion is an emotional bias that describes the tendency to prioritize avoiding losses over earning gains. Financial advisors say that investors across age groups exhibit this issue and make less prudent decisions with the intent of protecting themselves from downside. Source.

Schwab Asset Management

To be a good investor, one must have a strong command over one’s emotions. Billionaire investor Charlie Munger has repeatedly said that Emotional Quotient (“EQ”) is more important than Intelligence Quotient (“IQ”) to be a successful investor.

A lot of people with HIGH IQ’s are terrible investors, because they have terrible temperaments – Charlie Munger.

Sure, there appear dark clouds over the economy today, but try to think of a year in the past decade when Mr. Market didn’t have any concerns. Avoiding the markets altogether and hoarding cash (and cash equivalents) in fear of a recession is a decision made in poor judgment.

I am using the bear market sale to boost my income. A larger, more dependable passive income stream is the secret to achieving financial independence and early retirement. Two safe preferred picks with up to 8% yields for a magnificent retirement.

Be the first to comment